Alphabet (NASDAQ:GOOGL) Stock at $185 – Is AI and Cloud Growth Enough to Drive a Rally?

Google’s AI strategy, $75B CapEx, and YouTube’s ad boom—can NASDAQ:GOOGL break past $225, or is the stock still underpriced? | That's TradingNEWS

Alphabet Inc. (NASDAQ:GOOGL): Is the Tech Giant Undervalued or Poised for Major Growth?

Alphabet’s Dominance in Search and AI Integration

Alphabet Inc. (NASDAQ:GOOGL) remains an industry powerhouse, leveraging its deep-rooted dominance in search while aggressively pushing into artificial intelligence. Google Search continues to generate the majority of its revenue, with Q4 2024 search and related ad revenue climbing 12.5% year-over-year to $54 billion, proving that AI-driven competitors like ChatGPT have yet to make a significant dent in its advertising business. Despite rising competition in AI-generated search responses, Google’s ability to maintain strong user engagement through products like YouTube, Google Maps, and Google Assistant ensures that its advertising ecosystem remains robust.

The company’s integration of AI is a key driver of future growth. Gemini 2.0, Google’s latest AI model, is a step forward in multimodal AI, allowing it to process text, images, video, and audio simultaneously. This puts Google in direct competition with OpenAI and Microsoft, but Google has an edge—its massive dataset collected from billions of daily search queries and YouTube interactions. This extensive dataset gives it a superior foundation for training AI models, ensuring that its search business remains both dominant and increasingly AI-enhanced.

Google Cloud’s Growth Trajectory and AI Monetization

Google Cloud remains a critical component of the company's long-term strategy. Q4 revenue for the cloud segment hit $12 billion, a 30.1% year-over-year increase, showing that enterprise adoption of Google’s AI-powered cloud services is accelerating. While Amazon Web Services (AWS) and Microsoft Azure remain larger, Google Cloud’s AI integrations are attracting major clients, including Mercedes-Benz and Servier, who are looking to leverage generative AI for automation and decision-making processes.

One of the major catalysts for Google’s cloud business is its AI-driven enterprise solutions, particularly its ability to process large-scale PDFs, financial documents, and other complex data formats—an area where Gemini AI outperforms competitors in accuracy and cost-effectiveness. The multimodal capabilities of Gemini 2.0 make it an attractive option for businesses that need real-time document analysis, advanced speech-to-text, and AI-powered search within enterprise databases.

Alphabet’s $75 Billion CapEx Push: Is it a Risk or a Power Move?

Alphabet has committed to $75 billion in capital expenditures for 2025, a 40% increase from the $52.5 billion spent in 2024. This has caused concern among investors, as heavy spending in AI infrastructure could weigh on profitability in the short term. However, this spending is critical to maintaining Google’s AI lead.

A significant portion of this investment is being directed toward:

- AI-specific data centers that will handle the next generation of AI workloads, positioning Google as a leader in cloud-based AI solutions.

- TPU (Tensor Processing Unit) optimization, which allows Google to reduce the cost of AI model training compared to competitors relying on third-party GPUs from NVIDIA.

- Google Search’s AI integration, which is expected to increase user engagement and ad revenue through AI-powered summaries, recommendations, and interactive responses.

While Meta (META) plans to spend $65 billion and Microsoft (MSFT) will invest over $80 billion, Google’s strategy differs in that it is building both the AI models and the infrastructure needed to deploy them efficiently. This vertical integration gives Alphabet a cost advantage over OpenAI and Microsoft, which rely on external AI training solutions.

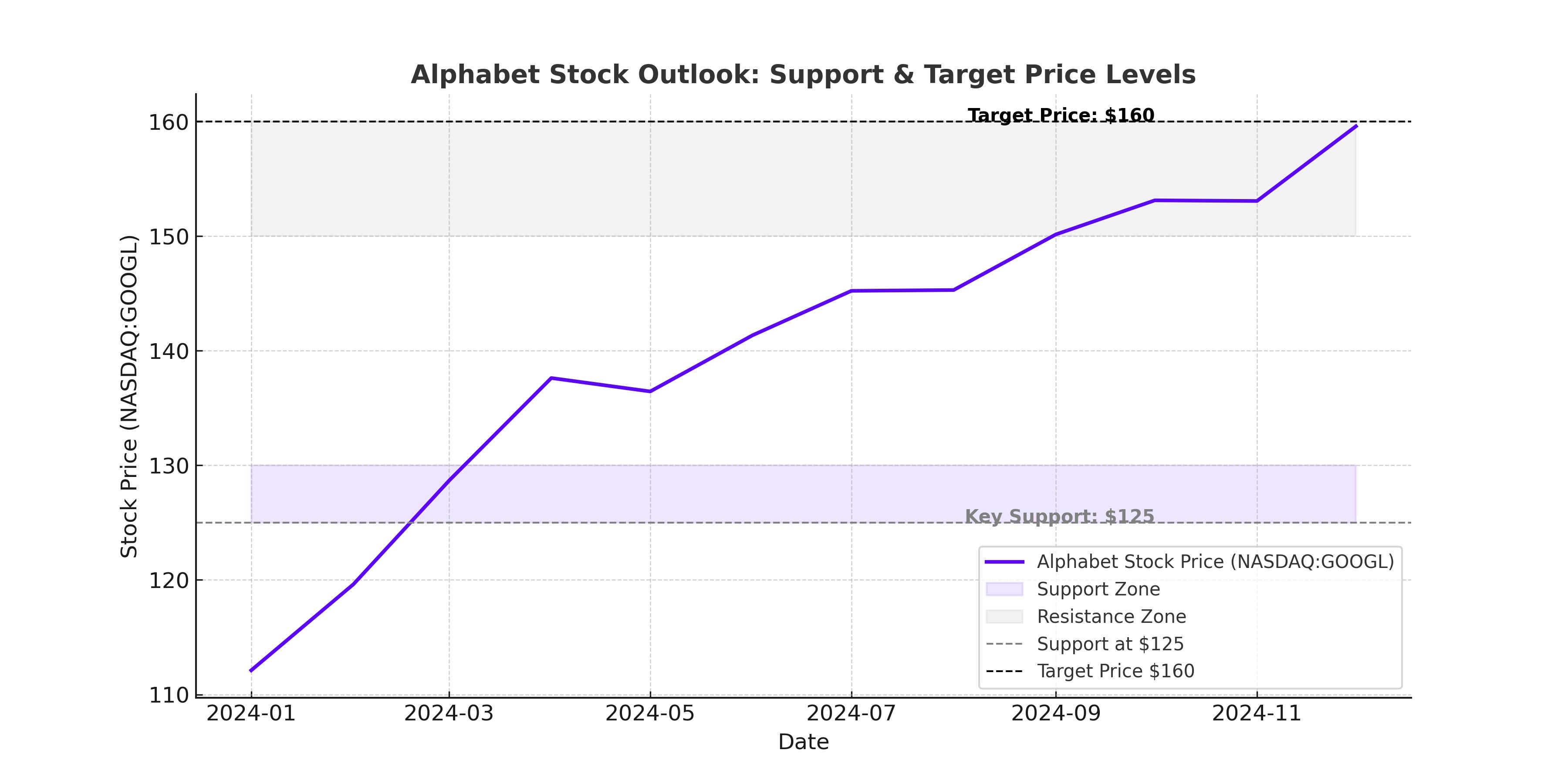

Valuation: Is Alphabet (NASDAQ:GOOGL) Undervalued?

Despite Google’s aggressive push into AI, the stock remains undervalued relative to its growth potential. Google is trading at a forward P/E ratio of 20.7, which is well below its 10-year average of 24.9. When adjusted for Alphabet’s $95.66 billion in cash reserves, the effective P/E multiple is closer to 20, making it significantly cheaper than its big tech peers like Microsoft and Amazon.

Compared to the broader communication services sector, Google’s forward P/E is just 4.74% above the median, yet its projected earnings per share (EPS) growth rate of 20.78% is nearly 280% higher than the sector average. This implies that Google’s stock should be trading at a 25% premium to the sector median, meaning a fair value P/E of 24.68—suggesting a potential upside of 19.34% from current levels.

With analysts forecasting diluted EPS growth of 10.7% in 2025, 14.3% in 2026, and 15.3% in 2027, Google could deliver a 60% cumulative total return by 2027 if it closes the valuation gap.

The YouTube and Digital Ads Growth Story

YouTube remains one of Google’s strongest assets, with ad revenue growing 13.8% year-over-year to $10.5 billion in Q4 2024. Nielsen data confirms that YouTube is the #1 streaming platform in the U.S., ahead of Netflix, Amazon Prime Video, and Disney+.

What makes YouTube particularly strong is Google’s AI-driven ad targeting. A recent Nielsen study found that AI-powered YouTube ad campaigns deliver a 17% higher return on ad spend compared to traditional ad placements. This means advertisers are willing to spend more on Google’s platforms, reinforcing the long-term strength of its ad business.

In addition to advertising, YouTube’s subscription business is expanding rapidly, with YouTube Premium and YouTube TV subscriber counts climbing. Google One, the company’s premium cloud storage and AI subscription offering, has also gained traction, positioning Alphabet as a major player in the subscription-based economy.

Alphabet’s AI Risks and Regulatory Challenges

While Alphabet is well-positioned for AI-driven growth, it faces several risks. The biggest is regulatory scrutiny, as U.S. and European regulators have intensified their focus on Google’s search monopoly and digital advertising dominance. The ongoing antitrust lawsuits could lead to changes in Google’s business practices, potentially impacting revenue from search and display ads.

Additionally, competition from Microsoft (NASDAQ:MSFT) and OpenAI remains a threat. While Google is investing heavily in AI, Microsoft’s partnership with OpenAI gives it a strong foothold in AI-driven enterprise applications, particularly through Azure AI integrations. However, Google’s first-party data advantage and superior ad ecosystem should provide a strong defense against Microsoft’s expansion into AI search and advertising.

Cybersecurity risks are another challenge. As one of the largest data-driven companies in the world, Google remains a prime target for cyberattacks. A major security breach could lead to user distrust, regulatory fines, and long-term reputational damage.

Insider Transactions and Share Buybacks

Google’s management continues to show confidence in the company’s long-term growth. Alphabet repurchased over $70 billion worth of shares in 2024, reducing the total share count by nearly 10% over the past five years. This aggressive buyback strategy provides a built-in return of approximately 2% per year for shareholders.

Insider transactions indicate no major selling activity, reinforcing management’s confidence in Google’s future prospects. Investors can track insider transactions through Google’s stock profile.

Buy, Sell, or Hold? Alphabet’s (NASDAQ:GOOGL) Investment Case

Alphabet’s dominance in search, YouTube’s growth, and AI monetization strategies make it one of the most compelling tech investments today. The company’s $75 billion AI investment is a strategic move that reinforces its competitive moat in both cloud computing and generative AI.

With a forward P/E of 20.7, strong cash reserves, and EPS growth expected to exceed 15% annually, the stock remains undervalued compared to its historical averages and peers. If Google’s AI integration leads to further margin expansion, the stock could see 25-30% upside over the next two years.

For long-term investors seeking exposure to AI, cloud, and digital advertising, Alphabet (NASDAQ:GOOGL) is a strong buy.