AMD Stock (NASDAQ:AMD) is Down 30% – Is This the Best AI Buy Before It Surges Again?

Can AMD (NASDAQ:AMD) Overtake Nvidia as AI Demand Explodes? | That's TradingNEWS

NASDAQ:AMD Stock Faces Major AI Growth Wave – Is It a Strong Buy Now?

Can NASDAQ:AMD Capitalize on AI Expansion and Beat Nvidia?

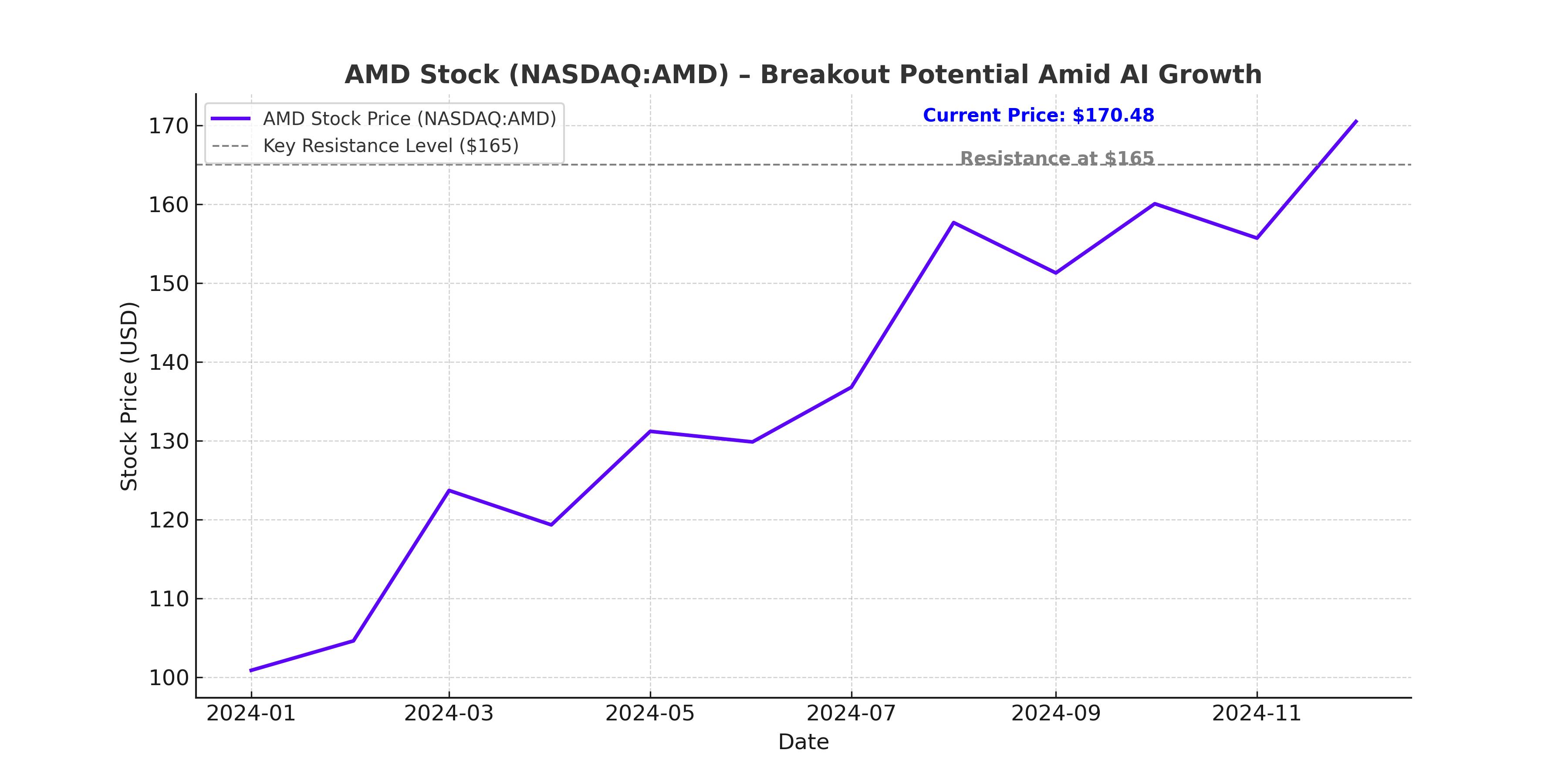

AMD (NASDAQ:AMD) has found itself at a critical turning point as AI computing demand explodes. The company, known for its high-performance processors, has aggressively expanded into the AI market, leveraging strategic partnerships with cloud giants like AWS, Microsoft Azure, and Google Cloud. With AI-driven data center revenue surging by 94% in FY2024, AMD’s positioning in the AI space has never been stronger. However, concerns around its software ecosystem, competitive pressures from Nvidia, and overall stock momentum after a six-month decline of nearly 30% have left investors questioning—is AMD a buy right now, or should investors wait for a deeper pullback?

AMD’s AI Expansion: Can It Challenge Nvidia’s Dominance?

AMD’s AI ambitions are clear. The company’s Instinct MI300X accelerators have positioned it as one of the few viable competitors to Nvidia’s H100 GPUs, the current industry leader in AI processing. AMD’s AI chip sales are expected to grow significantly in 2025, especially as AI agents such as OpenAI’s Deep Research begin to demand exponentially more inference power. Unlike traditional AI workloads that focus on single-question inference, Deep Research agents process continuous inference tasks, leading to significantly greater GPU demand.

AMD’s MI300X offers up to 192GB of high-bandwidth memory (HBM), compared to Nvidia’s H100 at 80GB and even the H200 at 141GB. This gives AMD a key advantage in workloads that require massive amounts of AI model storage on a single GPU, reducing latency and operational costs. For cloud providers looking for cost-efficient alternatives to Nvidia’s GPUs, AMD presents an increasingly attractive option.

In Q4 2024, AMD’s data center revenue soared 69% YoY to a record $3.9 billion, showing rapid adoption of its AI-focused hardware. With cloud hyperscalers set to invest over $300 billion into AI infrastructure in 2025, AMD is well-positioned to grab market share from Nvidia. However, the key challenge remains: Can AMD bridge the software gap and attract developers away from Nvidia’s CUDA ecosystem?

AMD’s Financial Strength: How Solid Are the Numbers?

AMD’s financial health remains strong, giving it the flexibility to invest aggressively in AI expansion. The company ended FY2024 with $2.8 billion in net cash, even after spending $6.5 billion on R&D, a 10% increase YoY. This level of spending highlights AMD’s commitment to long-term innovation and competition in AI hardware.

Revenue for Q1 2025 is projected to hit $7.1 billion, a 30% YoY increase, with EPS expected to surge by 51.3% YoY. This growth is fueled primarily by AI demand, with analysts predicting that AI-specific revenue could reach $3 billion annually by 2026.

Despite strong earnings, AMD’s stock momentum has been weak. The stock has declined nearly 30% in the last six months, with Wall Street analysts lowering their ratings. The key concern is that Nvidia’s dominance in AI accelerators is still too strong, and AMD’s reliance on ROCm, its alternative to CUDA, is not yet fully mature.

Is AMD’s AI Strategy Enough to Offset Weakness in Gaming and Embedded Segments?

Beyond AI, AMD still relies on gaming and embedded chip sales, which have faced significant headwinds. In FY2024, gaming revenue dropped, reflecting the cyclical decline in PC and console sales post-pandemic. The Embedded segment also shrank due to supply chain disruptions, but this is expected to recover as inventory levels stabilize.

Gaming remains a vital part of AMD’s revenue mix, and while short-term softness exists, analysts expect a 10.2% CAGR for the global gaming market through 2030. If AMD can capitalize on the next console refresh cycle and continued PC gaming growth, this segment should rebound.

Valuation: How Does AMD Compare to Nvidia?

AMD’s valuation looks much more attractive than Nvidia’s at current levels. While Nvidia trades at a forward P/E of 43, AMD’s forward P/E sits closer to 32, making it far cheaper relative to growth expectations. Analysts project AMD’s EPS to grow at a 23% CAGR over the next three years, supporting strong free cash flow growth.

Using a discounted cash flow (DCF) model, AMD’s fair value is estimated at $248 billion, compared to its current market cap of $180 billion. This implies 38% upside potential, even assuming conservative growth estimates.

If AMD’s AI strategy accelerates, the stock could move even higher, especially as more cloud providers diversify away from Nvidia.

Key Risks: Can AMD Maintain Its AI Momentum?

While AMD is well-positioned, several risks remain. Nvidia’s aggressive innovation cycle means that new GPUs could neutralize AMD’s hardware advantages. Additionally, Nvidia has a far more mature software ecosystem, and most AI developers are still using CUDA over AMD’s ROCm.

Another challenge is competition from Intel, which is trying to gain AI market share with its Gaudi accelerators and Xeon AI-focused chips. Large cloud providers such as Google and Amazon are also developing their own AI chips, which could limit AMD’s total addressable market in AI.

However, AMD’s growing partnerships with cloud giants, strong financial position, and competitive AI pricing strategy suggest that it remains a viable alternative to Nvidia’s more expensive AI solutions.

Final Verdict: Is NASDAQ:AMD a Buy, Sell, or Hold?

AMD remains a strong long-term buy, particularly for investors who believe in the AI revolution and its impact on data center computing. The stock’s recent weakness presents an opportunity for long-term investors, given its attractive valuation, strong growth outlook, and increasing market share in AI.

The biggest risks remain competition from Nvidia, software ecosystem challenges, and short-term market sentiment, but long-term AI-driven growth outweighs these concerns.

If AMD successfully expands its AI accelerator footprint and bridges the software gap, the stock could rally toward $200+ in the next 12-18 months. At the current price, long-term investors should consider AMD a strong buy.

Track AMD’s Live Stock Performance

That's TradingNEWS

Read More

-

GPIX ETF At $52.52: 8% Yield And Dynamic S&P 500 Income Upside

13.12.2025 · TradingNEWS ArchiveStocks

-

XRP ETFs Surge Toward $1B As XRPI Hits $11.64 And XRPR $16.48 With XRP Near $2

13.12.2025 · TradingNEWS ArchiveCrypto

-

Natural Gas Price Forecast: NG=F Hovers Near $4.07 Support After 22% Weekly Slide

13.12.2025 · TradingNEWS ArchiveCommodities

-

USD/JPY Price Forecast - Dollar to Yen at 154–158 Range as BoJ 0.75% Hike and Fed Cut Debate

13.12.2025 · TradingNEWS ArchiveForex