Baidu (NASDAQ:BIDU): Can the Chinese Tech Giant Rebound Amid Macro Challenges and Emerging Opportunities?

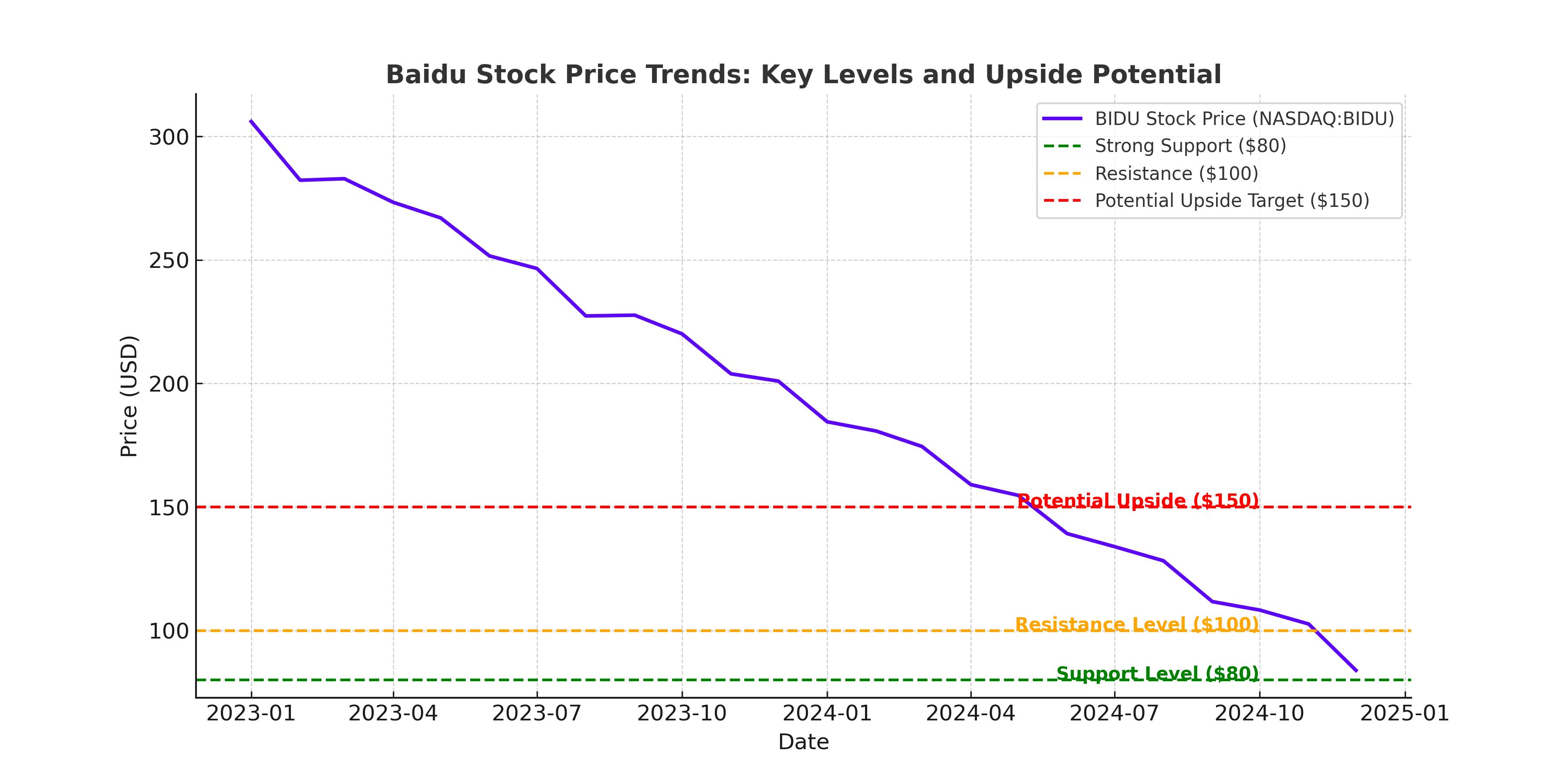

Baidu, Inc. (NASDAQ:BIDU), often referred to as the "Google of China," has faced a turbulent few years. However, its core business remains resilient, supported by a dominant position in China’s search engine market, strategic investments in AI and autonomous driving, and a robust free cash flow generation. As of today, shares of Baidu are trading at approximately $84, significantly below their peak valuation of $300 in 2021. With the recent implementation of stimulus measures by the Chinese government and a tightening base near $80, investors are left questioning whether this is the moment to buy into Baidu's recovery story.

Baidu’s Core Business: Resilient Despite Revenue Challenges

Baidu’s primary revenue stream, digital advertising, accounted for over 70% of its total revenue in 2024. Despite a sluggish Chinese economy that grew at only 5%, Baidu managed to maintain a healthy EBITDA margin of 31% in Q3 2024, comparable to 32% in the same period a year prior. This resilience underscores the strength of its search engine business, which commands a 45% market share in China. However, revenue growth in this segment was stagnant in Q3 2024, reflecting broader economic pressures.

The advertising market in China has struggled to regain momentum post-COVID, with consumer spending remaining weak. Baidu’s ability to preserve profitability despite these challenges is a testament to its efficient cost management and the high-margin nature of its digital advertising business.

The Stimulus Impact: A Potential Tailwind for Baidu

In late 2024, Beijing introduced a massive $1.4 trillion (10 trillion yuan) stimulus package to revitalize its slowing economy. This package included easing lending restrictions, lowering mortgage rates, and addressing debt issues in the real estate sector. While these measures were primarily aimed at stabilizing the housing market, they also have broader implications for consumer and corporate spending. For Baidu, a recovery in consumer confidence and spending power could translate into higher advertising revenue, as businesses ramp up their marketing efforts.

Additionally, sectors like technology, which are closely linked to consumer sentiment and corporate investment, stand to benefit significantly from these stimulus efforts. Baidu’s dominant position in the search and digital advertising space makes it well-positioned to capture this upside.

Free Cash Flow and Shareholder Returns

Baidu’s ability to generate free cash flow remains a critical component of its investment thesis. In Q3 2024, Baidu generated 2.6 billion yuan ($376 million) in free cash flow, representing an 8% margin. This strong cash generation has allowed Baidu to return capital to shareholders through an ongoing $5 billion stock buyback program initiated in 2023. By the end of Q3 2024, Baidu had repurchased $1.4 billion worth of shares, with $161 million repurchased in the most recent quarter.

Looking ahead, Baidu’s strong free cash flow positions it to continue these buybacks in 2025, offering a potential catalyst for share price appreciation. The company's disciplined approach to capital allocation is particularly attractive in a market where many tech companies are struggling to balance growth and profitability.

AI and Autonomous Driving: The Next Frontier

Baidu has invested heavily in artificial intelligence (AI) and autonomous driving, positioning itself as a leader in these high-growth markets. The company’s Apollo autonomous driving platform continues to make strides, with over 1 million test miles completed and partnerships established with leading automakers. In 2024, Baidu’s Apollo Go service expanded its operations to additional cities in China, with plans to cover 65 cities by 2025.

While these initiatives are still in the early stages of monetization, they represent a significant long-term growth opportunity for Baidu. The global autonomous vehicle market is projected to grow at a compound annual growth rate (CAGR) of 22.7% through 2030, offering a substantial runway for Baidu to capitalize on its early investments.

Valuation: Deeply Discounted with Significant Upside

Baidu is currently trading at a forward price-to-earnings (P/E) ratio of 7.5x based on FY 2026 earnings estimates of $10.22 per share. This represents a significant discount to both its historical average P/E of 14.5x and the broader market. By comparison, Alibaba (BABA), another major Chinese tech player, trades at a forward P/E of 8.8x. Baidu’s valuation implies an earnings yield of 13%, highlighting the stock’s attractiveness for value-oriented investors.

Based on a conservative fair value P/E of 14.5x, Baidu shares could be worth approximately $150, representing an upside potential of nearly 80% from current levels. This valuation assumes stable profitability in the core advertising business and continued free cash flow generation.

Risks: Navigating Uncertainty in China

Investing in Baidu comes with inherent risks, primarily related to its exposure to China’s economic and regulatory environment. The Chinese government’s influence on large tech companies remains a key concern for investors, as does the geopolitical tension between the US and China. Additionally, Baidu’s reliance on digital advertising means that any prolonged weakness in this market could weigh on its financial performance.

Another risk is the pace of monetization for Baidu’s investments in AI and autonomous driving. While these initiatives have significant potential, they require substantial upfront investment and face competition from both domestic and international players.

Technical Analysis: Strong Support Levels

Baidu’s stock has found strong support near the $80 level, with technical indicators suggesting a potential breakout above its 200-day moving average. The consolidation in recent months has created a solid base, and any positive news—whether from earnings or macroeconomic developments—could serve as a catalyst for a sustained rally.

Final Take: Is NASDAQ:BIDU a Buy?

Baidu offers a compelling investment opportunity for those willing to navigate the complexities of the Chinese market. Its dominant position in search, robust free cash flow, and undervaluation provide a strong foundation for future growth. While risks remain, the upside potential—driven by stimulus measures, AI advancements, and shareholder returns—makes NASDAQ:BIDU an attractive play for long-term investors. With shares trading at just $84, Baidu could be a hidden gem in a challenging market environment. Investors should monitor key developments, including earnings reports and updates on its AI and autonomous driving initiatives, to gauge the company’s progress toward unlocking its full value potential.