BP p.l.c. (NYSE:BP): Is This the Energy Stock Investors Should Bet On in 2025?

BP’s Strategic Shift: Can It Unlock Hidden Value for Shareholders?

BP p.l.c. (NYSE:BP) has seen its stock struggle, significantly underperforming its European and U.S. peers over the past three years. The stock has lagged behind Exxon Mobil (NYSE:XOM), Chevron (NYSE:CVX), and Shell (NYSE:SHEL) since 2021, and Q4 2024 earnings have dropped to the lowest levels since the crisis-driven quarters of 2020. Yet, despite this poor performance, BP remains one of the most undervalued major energy companies, trading at just 3.1x EBITDA and offering a free cash flow (FCF) yield of approximately 15%. With a combination of dividends and buybacks returning over 13% to shareholders, the question is: Can BP finally close the valuation gap and regain investor confidence?

BP's Weak Q4 Earnings: What Went Wrong?

BP's fourth-quarter results disappointed, with profits plummeting 61% year-over-year, coming in at just $1.169 billion. The main culprits? A decline in petroleum prices and refining margins, as well as weak performance in BP’s trading division. The company's refining marker margin plunged 20% quarter-over-quarter to $13.1 per barrel, the lowest since early 2022. In contrast, Shell and TotalEnergies (NYSE:TTE) both reported stable or improved refining margins in their latest earnings updates, making BP’s performance even more concerning.

Production also took a hit, with both crude oil and natural gas volumes declining due to turnarounds and maintenance activity. The downstream segment saw lower refining throughput and weaker fuel sales, driven by seasonally weaker demand. On top of that, BP’s oil and gas trading desks underperformed, with natural gas trading coming in at “average” and oil trading described as “weak.” These combined factors dragged down EBIT by roughly 15%, landing at approximately $4.4 billion for the quarter.

Investor Day: A Make-Or-Break Moment for BP?

All eyes are now on BP’s upcoming investor day on February 26, 2025, where CEO Murray Auchincloss is expected to outline a new strategic direction. BP is rumored to be abandoning its previous target of cutting oil production by 25% by 2030, signaling a dramatic shift back toward fossil fuel investments. This could mirror the strategy change at Shell, which helped reignite interest from investors who had grown frustrated with the European energy giant’s aggressive push into renewables.

BP has already made some key moves, including laying off 5% of its workforce and reorganizing its offshore wind operations into a 50/50 joint venture with Japan’s JERA. However, a major issue remains: The investor presentation was originally planned for New York but was moved to London. This could be a missed opportunity, as U.S. investors are far more willing to allocate capital to oil and gas companies than European funds, which are often restricted from investing in traditional energy stocks due to ESG mandates.

BP’s Capital Allocation: Are Shareholders Finally Getting Rewarded?

Despite weak earnings, BP has continued to reward investors through aggressive share buybacks and dividends. The company repurchased $1.75 billion in stock during Q4, bringing its full-year 2024 buybacks to $7 billion. An additional $1.75 billion buyback has already been announced for early 2025. Meanwhile, BP reduced net debt by $1 billion in Q4, a sign that it is maintaining financial discipline even amid earnings volatility.

At current levels, BP is yielding an astonishing 15% in free cash flow—the highest among all supermajors. It also offers a 13% shareholder return when combining its 6% base dividend yield and buybacks. In contrast, Exxon Mobil and Chevron are returning roughly 7-8% to shareholders. However, while BP offers the most compelling yield, investor sentiment has remained weak, keeping valuations suppressed.

BP’s Valuation: Is the Stock Too Cheap to Ignore?

BP remains deeply undervalued compared to its peers. The stock currently trades at just 3.1x EBITDA and 9.0x forward earnings, compared to Exxon’s 12.7x P/E and Chevron’s 12.5x P/E. Even Shell, which has faced similar challenges in Europe, is trading at 8.3x forward earnings, while BP remains at a discount.

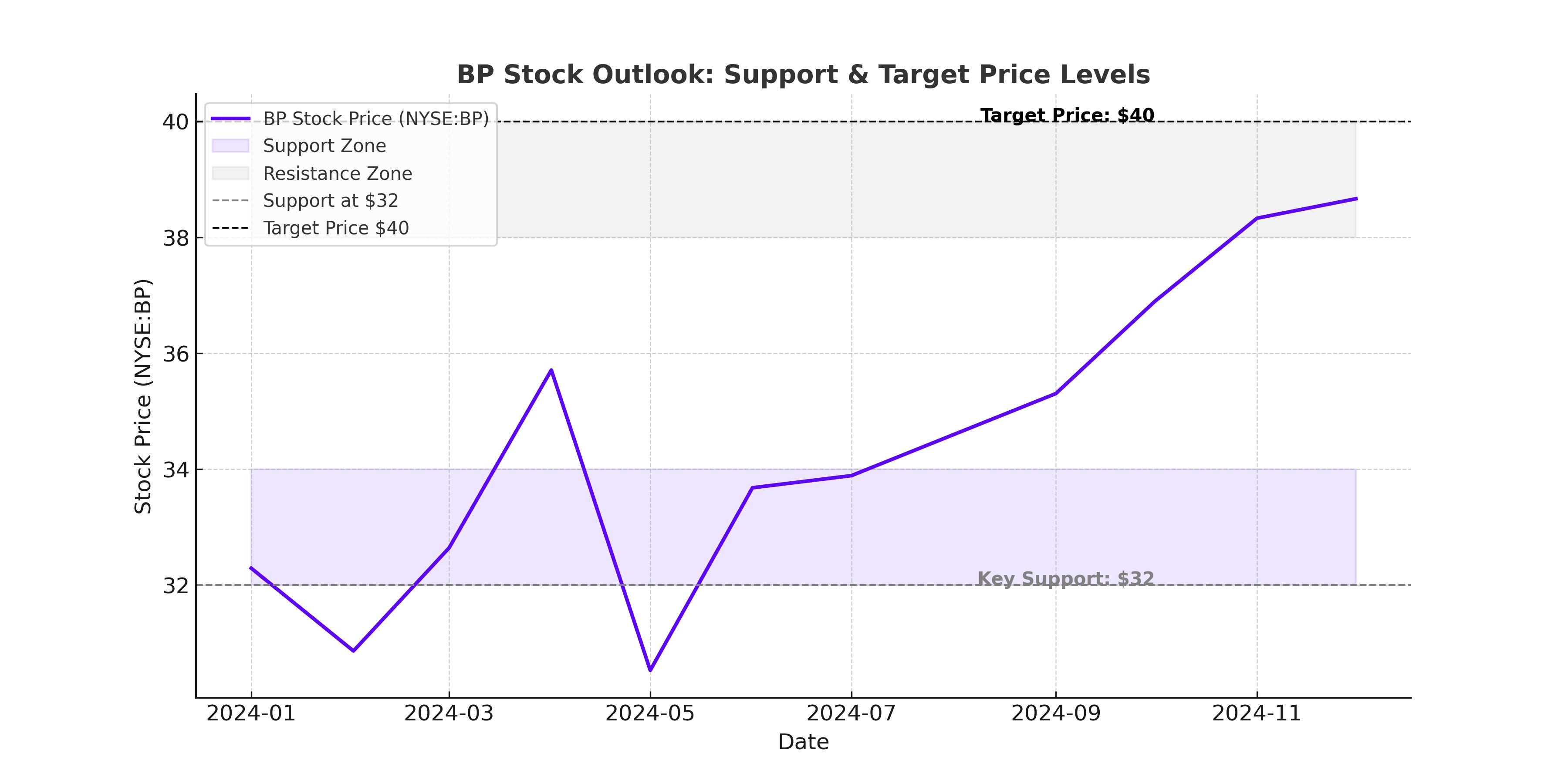

If BP successfully executes its strategy shift and convinces investors that it is serious about prioritizing high-return oil and gas assets over underperforming renewable ventures, the stock has significant re-rating potential. A 12x earnings multiple, in line with its U.S. peers, would imply a fair value of $38 to $46 per share, representing a 30-50% upside from current levels.

The Elliott Management Factor: Will Activist Pressure Force Change?

Activist hedge fund Elliott Management has taken a $5 billion stake in BP, making it one of the company’s largest shareholders. Elliott has a long history of pushing for major strategic overhauls at underperforming companies, including energy giants. The hedge fund is likely to push BP to divest low-margin assets, focus on high-return projects, and increase capital returns to shareholders.

Elliott’s involvement is a strong catalyst for change and could accelerate a major corporate restructuring at BP. The investor day later this month will provide clues as to how much influence Elliott has on the boardroom. If BP signals higher oil production targets, more aggressive buybacks, and divestitures of non-core assets, expect significant upside potential for the stock.

What Could Go Wrong? Key Risks for BP Investors

BP remains highly sensitive to oil price fluctuations. While crude has stabilized in the $70 per barrel range, any unexpected downturn in prices could pressure earnings and slow buybacks. Additionally, if BP fails to execute its strategy shift effectively, investor skepticism will remain, keeping valuations depressed. The company’s history of underperformance relative to peers is another risk factor, and management needs to deliver a clear, decisive plan at its investor day to restore confidence.

Final Verdict: Is BP Stock a Buy?

BP remains one of the most undervalued global energy giants, with significant upside potential if it successfully executes its strategy reset. The upcoming investor day is a pivotal moment that could determine the company’s future trajectory. With 15% free cash flow yields, 13% shareholder returns, and activist pressure from Elliott Management, BP has all the ingredients for a major turnaround story.

If management commits to prioritizing high-margin oil and gas assets, announces higher production growth targets, and accelerates share buybacks, BP stock could easily re-rate 30-50% higher over the next 12 months. However, execution risk remains