Meta Stock Rockets to $725 – Is NASDAQ:META Still a Buy or Is It Overheated?

With AI-driven ad revenue soaring and Reality Labs bleeding $20B, can Meta (NASDAQ:META) justify its valuation? Or is the stock running out of steam? | That's TradingNEWS

Meta Stock (NASDAQ:META) Rockets Past $725 – Can It Keep Climbing or Is a Correction Coming?

Meta Platforms (NASDAQ:META) Is Surging, But How Much More Upside Is Left?

Meta Platforms (NASDAQ:META) has been on a relentless rally, now trading at an astonishing $725 per share. The social media and AI powerhouse continues to dominate the digital advertising industry, driving massive revenue growth and expanding its profit margins. But with such an aggressive run-up in share price, the critical question investors are asking is: Can Meta sustain this momentum, or is a pullback inevitable?

After a blockbuster 2024, where Meta delivered a 21% YoY revenue increase and an EPS surge of 50%, investors have been piling into the stock. Advertising revenue continues to be the backbone of Meta’s success, with the price per ad jumping 14% YoY, reflecting stronger AI-driven targeting and increased advertiser demand. However, despite this impressive growth, Meta’s massive AI infrastructure investments and the continued losses in Reality Labs—now surpassing $20 billion annually—are raising concerns about long-term profitability.

The recent earnings report showcased how Meta has successfully monetized its enormous capex, leading Wall Street to favor its AI strategy over competitors like Alphabet (NASDAQ:GOOGL) and Microsoft (NASDAQ:MSFT). Unlike Alphabet, which saw a negative reaction to increased spending, Meta’s investment in AI and advanced ad tools has directly boosted its bottom line, making the market more forgiving of its high spending.

Is NASDAQ:META’s Ad Business Strong Enough to Keep Driving Growth?

A key reason behind Meta’s surge is the company’s ability to consistently increase ad pricing while maintaining high engagement levels across its platforms, including Facebook, Instagram, and WhatsApp. In Q4 2024, ad impressions grew by 6% YoY, and the average price per ad surged 14%, demonstrating the effectiveness of AI-driven ad placement. The company’s ad revenue hit $47.3 billion, a massive leap from $39 billion in the previous year.

Despite this, there are emerging risks. Digital ad spending has been booming, but there are signs of a potential slowdown in 2025. Political ad spending, which was a significant driver in 2024 due to elections worldwide, will likely decline. Additionally, global economic uncertainties and tightening consumer spending could lead to weaker advertising growth, impacting Meta’s top-line expansion.

Another critical factor to watch is whether Meta can sustain its dominance in the social media ad market. While platforms like TikTok and Snapchat (NYSE:SNAP) pose competition, Meta’s vast user base of 3.35 billion daily active people provides an unmatched scale for advertisers. The question remains: Can Meta continue raising ad prices without pushing advertisers toward cheaper alternatives?

Meta's AI Bet: A Competitive Advantage or a Cash Drain?

Meta’s aggressive investment in artificial intelligence has become a defining theme for the company. CEO Mark Zuckerberg has committed $60-$65 billion in capex for 2025, primarily focused on AI infrastructure. The company now operates over 1.3 million GPUs, making it one of the most AI-driven enterprises globally.

This massive investment is aimed at improving ad personalization, building AI chatbots, and powering Meta’s Llama 4 large language model. Llama 4 is expected to rival OpenAI’s GPT models, offering a cost-effective alternative to high-end AI solutions. The question now is: Will Meta’s AI dominance translate into long-term revenue growth, or is it an unsustainable cash burn?

Investors have reacted positively to Meta’s AI push, particularly in contrast to Alphabet, which faced heavy selling after announcing higher AI spending. However, there is still skepticism over whether Meta can monetize these AI investments beyond advertising. AI-powered assistants and AI-driven content creation tools have potential, but they remain largely unproven revenue drivers.

Reality Labs: A $20 Billion Bet That Still Has No Payoff

While Meta’s core ad business is thriving, its Reality Labs division continues to bleed cash. The company reported a $4.96 billion loss in Reality Labs for the latest quarter, bringing its total annualized loss to nearly $20 billion.

Reality Labs, which houses Meta’s AR/VR initiatives and metaverse projects, generated just $1.08 billion in revenue, representing a mere 1% YoY growth. Given the staggering losses, many investors are questioning whether Meta should continue pouring billions into this division.

The competitive landscape is also heating up. Samsung and Google have recently announced an Android-based XR headset, directly challenging Meta’s Quest lineup. Meanwhile, Apple’s Vision Pro is positioning itself as the premium AR/VR device, potentially limiting Meta’s ability to dominate the market.

Despite the continued losses, Meta sees Reality Labs as a long-term play. The company believes owning the hardware and platform will allow it to bypass reliance on Apple’s ecosystem, ensuring more direct monetization opportunities. However, with no clear profitability timeline, how long can Meta afford to sustain these losses before investors demand a shift in strategy?

Is Meta Stock Still Undervalued Compared to Other Big Tech Giants?

Despite the massive rally, Meta’s valuation remains relatively attractive compared to its peers. The company’s forward P/E ratio for 2026 is 24.2, significantly lower than Apple’s 28x forward earnings multiple.

Meta has also outpaced Apple in revenue growth over the last two years, making it a more attractive investment based on earnings expansion. Apple has struggled with declining iPhone sales and slower services growth, while Meta continues to show robust ad revenue growth and expanding profit margins.

Wall Street’s current projections put Meta’s 2025 operating profit above $100 billion, a substantial jump from $69.4 billion in 2024. This makes Meta one of the most profitable companies in the world, with significant room for multiple expansion if the company can maintain its growth trajectory.

Will NASDAQ:META Hit $800 or Face a Pullback?

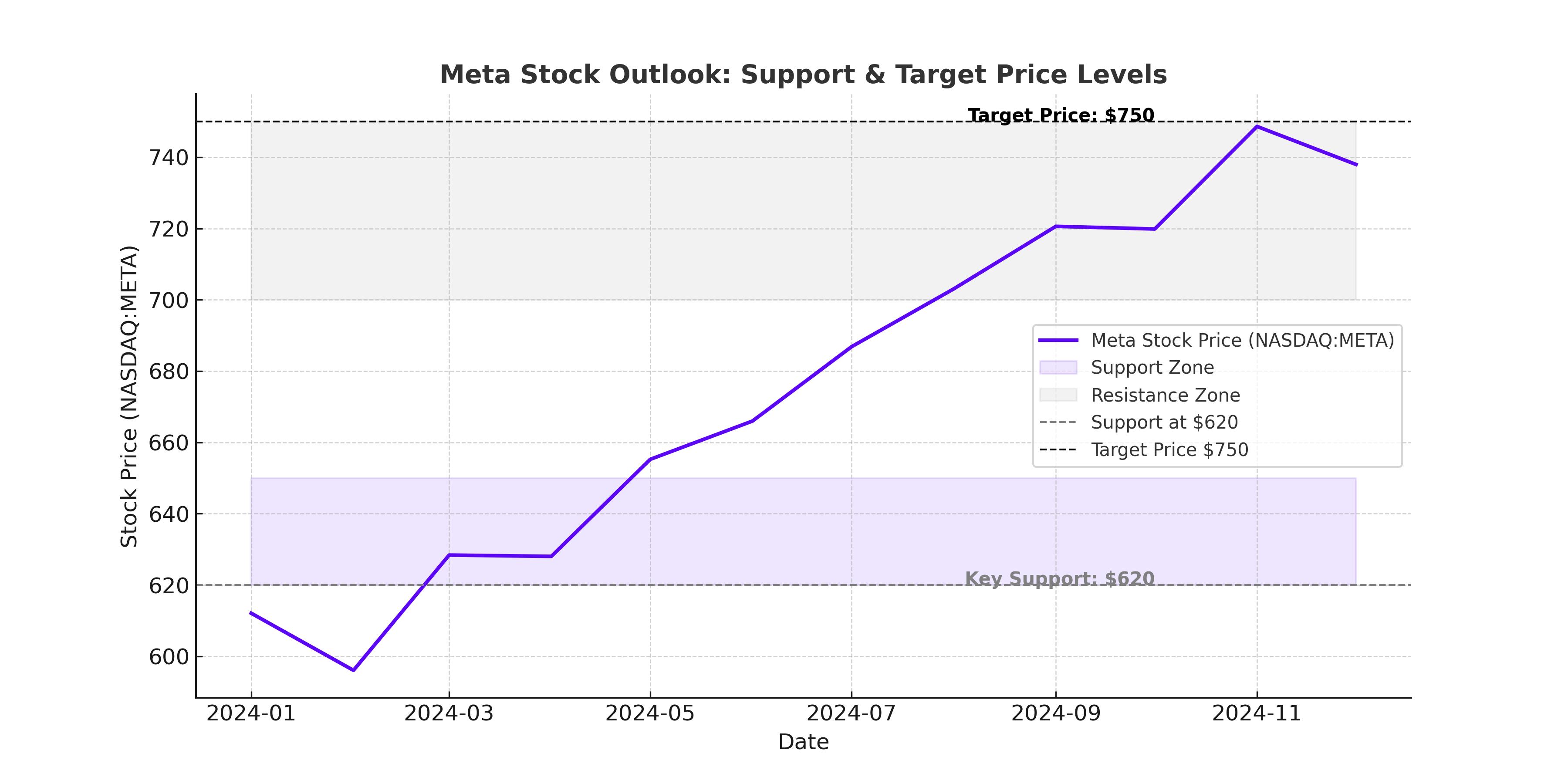

The biggest question for investors now is whether Meta’s rally can continue, or if the stock is due for a correction. Historically, such rapid stock gains are often followed by short-term pullbacks. However, if Meta can continue delivering strong ad revenue growth, maintain its AI leadership, and show progress in Reality Labs, the stock could push beyond $800 per share in the coming months.

On the flip side, any slowdown in ad spending, increased AI competition, or continued heavy losses in Reality Labs could trigger a pullback. Investors should watch key levels, including the $700 support zone and resistance at $750-$775.

Meta remains a dominant force in digital advertising, but the AI-driven future is still uncertain. With a reasonable valuation and strong financials, the stock remains a compelling buy, though cautious investors may wait for dips before adding to their positions.