Micron (NASDAQ:MU) Surges on AI Boom—But Is the Stock Overpriced or Still a Buy?

Is Micron’s AI-driven DRAM Demand Enough to Sustain Its Rally, or Will Competition Drag It Down? | That's TradingNEWS

Micron Technology (NASDAQ:MU): Navigating the Memory Market and AI Boom

Micron's Growth Trajectory: Is NASDAQ:MU a Buy at Current Levels?

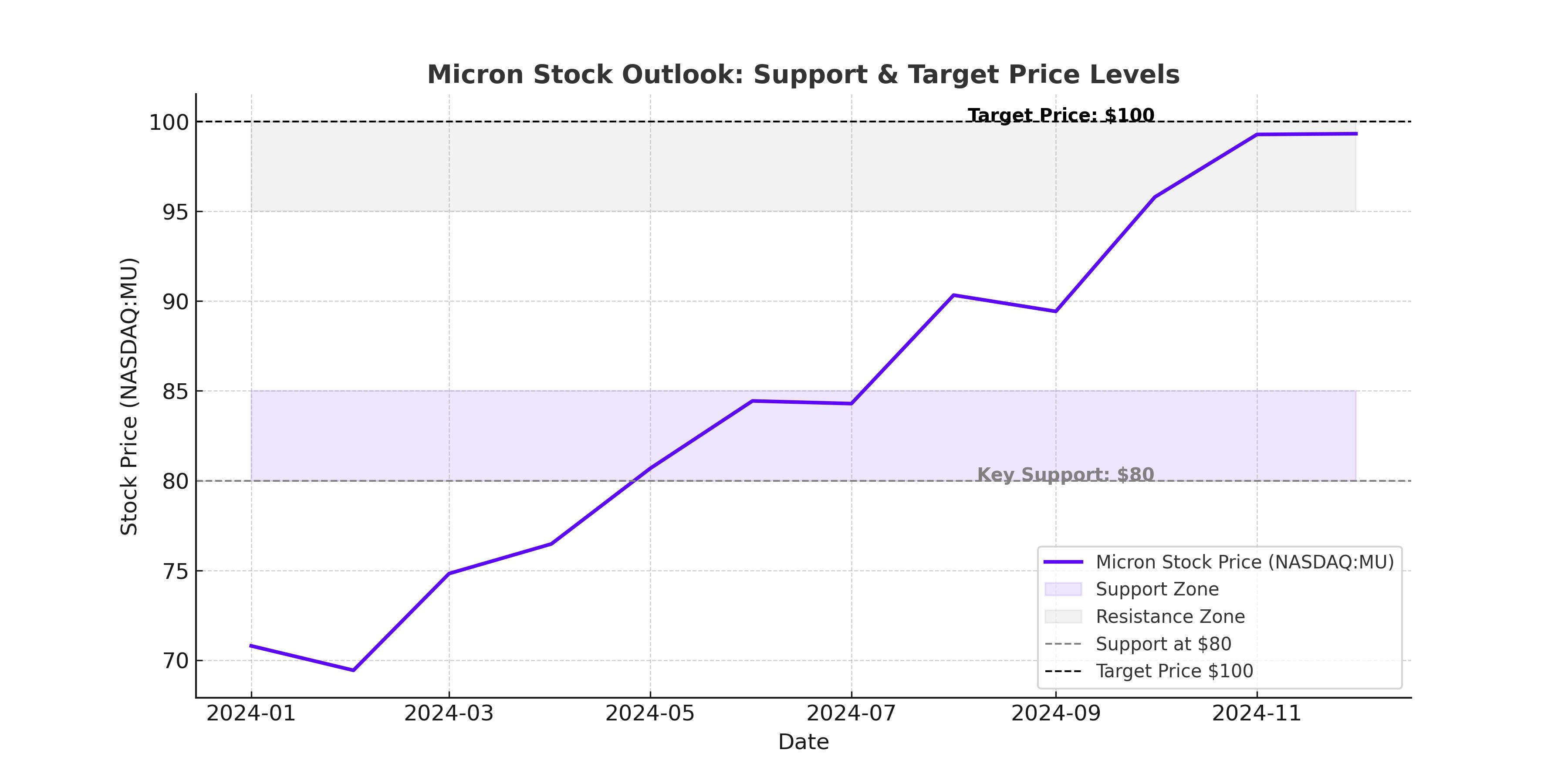

Micron Technology (NASDAQ:MU) has been on a significant upswing, driven by soaring demand for high-bandwidth memory (HBM) chips used in artificial intelligence (AI) applications. The stock is currently trading around $93.41, reflecting a 40% increase year-to-date, with investors eyeing the company’s ability to capitalize on the AI-driven semiconductor boom. However, risks remain, including cyclical downturns in memory pricing, competition from South Korean giants like Samsung and SK Hynix, and ongoing geopolitical uncertainties.

With the AI industry growing exponentially and Micron securing high-profile partnerships with NVIDIA (NASDAQ:NVDA) for HBM chips, the question remains: Can Micron sustain its momentum, or is the stock already priced in for perfection?

AI Boom and Micron’s Role in the Next Computing Era

Micron has positioned itself as a leader in memory and storage solutions, with HBM chips playing a critical role in AI acceleration. With NVIDIA’s Blackwell GPUs launching in 2025, the demand for HBM3 and HBM3E memory solutions is expected to surge, and Micron is poised to benefit. The company has already secured orders from NVDA, adding significant revenue visibility for the next 12-18 months.

Micron’s HBM production is ramping up, with the company set to deliver HBM3E shipments by mid-2025, placing it ahead of competition in delivering next-gen AI memory solutions. This is a crucial differentiator, as AI training and inference workloads require faster and more efficient memory solutions.

Memory Market Rebound: Are DRAM and NAND Flash Prices Stabilizing?

After a brutal two-year downturn, the memory chip market is finally seeing a resurgence. DRAM prices have surged over 25% in the last six months, while NAND prices are up 18% from their Q3 2024 lows. Micron, which derives approximately 70% of its revenue from DRAM and 25% from NAND, is set to benefit from this cyclical rebound.

However, the ongoing pricing war between Micron, Samsung, and SK Hynix remains a factor to watch. While supply cuts by competitors have helped stabilize pricing, Samsung has signaled it may increase production in late 2025, potentially leading to price pressures.

Earnings Expectations: Will Micron Beat Estimates Again?

Micron’s Q2 2025 earnings are expected to show a substantial improvement, with analysts projecting revenue of $7.6 billion, marking a 35% year-over-year increase. Gross margins are expected to expand to 35%, up from 24% last quarter, as higher HBM shipments contribute to improved profitability.

Key metrics to watch in the upcoming earnings report:

- DRAM ASP Growth: A continuation of the 10-15% sequential increase could drive higher revenues.

- HBM Shipment Updates: Investors will look for more clarity on HBM3E production and orders from NVIDIA.

- NAND Pricing Stability: A sharp decline could negatively impact margins.

Geopolitical Risks: China’s Impact on Micron’s Revenue Stream

China remains a double-edged sword for Micron. The company generates over 15% of its revenue from China, but ongoing U.S. sanctions on chip exports pose risks. Micron has been caught in the crossfire between the U.S. and China, with Beijing restricting some sales to Chinese firms in retaliation for U.S. export bans.

While Micron has successfully diversified its supply chain, including shifting focus to Taiwan and Japan, investors need to monitor further geopolitical developments. If China expands its restrictions, it could erase billions in potential revenue for Micron.

Micron’s Valuation: Is the Stock Overpriced?

At a forward P/E of 21x, Micron is no longer a deep-value play, but its valuation remains attractive relative to AI peers like NVIDIA (44x forward P/E) and AMD (38x forward P/E).

The key question: Is MU still a buy at current levels, or has the AI memory boom been priced in?

Insider Transactions: What Are Micron Executives Doing?

Micron’s insider transactions reveal an interesting trend. In the past three months, insiders have sold approximately $20 million worth of shares, signaling potential caution at current levels. However, institutional buying remains strong, with hedge funds increasing positions in anticipation of stronger AI-related growth.

For detailed insider transaction data, check Micron Insider Transactions.

Final Verdict: Buy, Hold, or Sell?

Micron Technology remains one of the best-positioned semiconductor stocks for AI growth, with its HBM leadership and DRAM pricing recovery fueling optimism. However, geopolitical risks, potential supply increases from Samsung, and high insider selling warrant caution.

The stock is not cheap, but given its exposure to AI, long-term growth potential remains strong. Investors should watch the upcoming earnings report for guidance on HBM shipments and pricing trends before making a decision.

Recommendation: Hold for now, Buy on any earnings-related dip.

For real-time Micron stock updates, visit Micron Real-Time Chart.