NASDAQ:AMD – Is AMD Stock Undervalued Amid AI Growth?

AMD's 45% Decline – A Buying Opportunity or a Warning Sign?

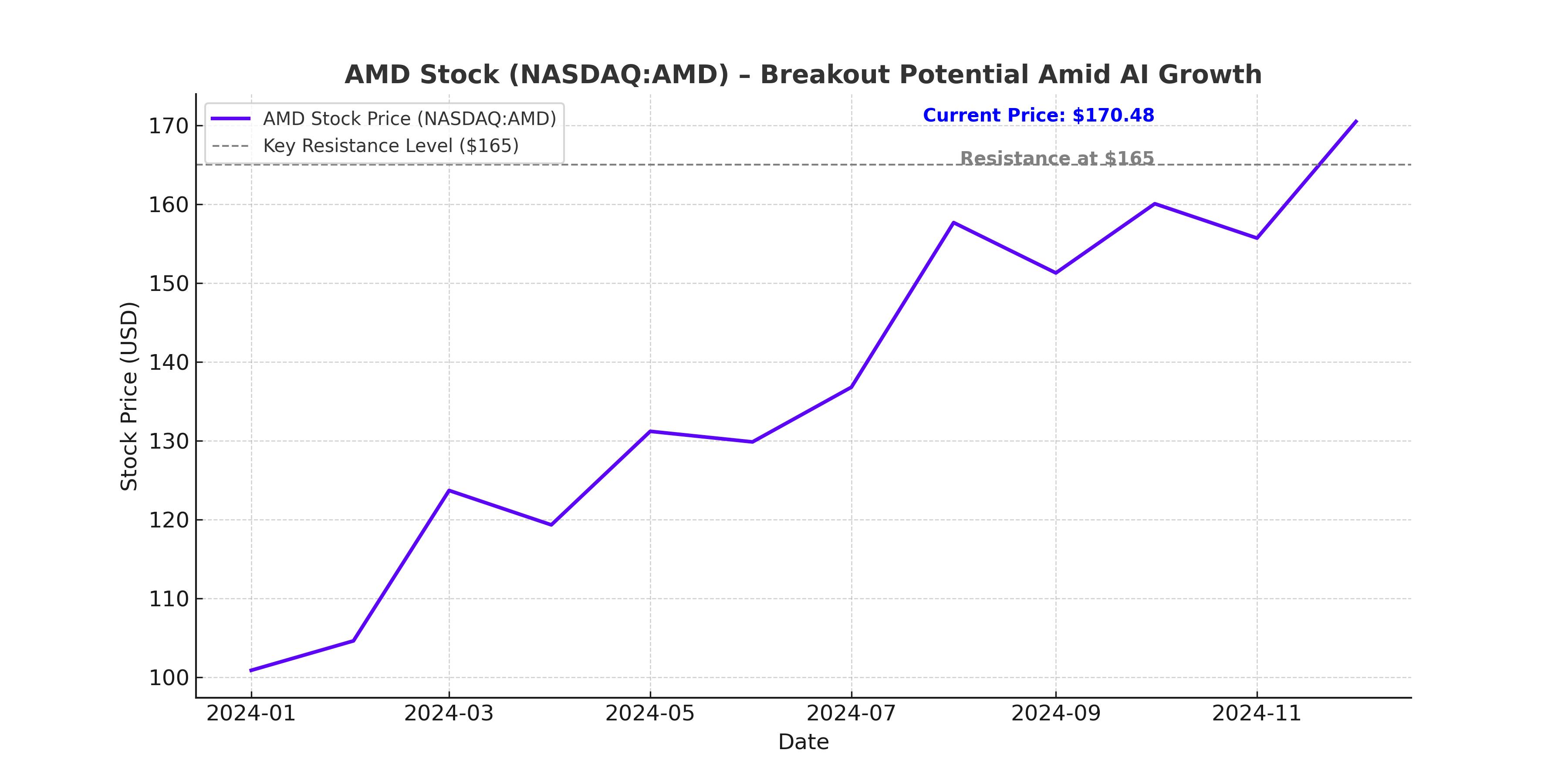

Advanced Micro Devices (NASDAQ:AMD) has suffered a sharp 45% decline from its peak in early 2024, significantly underperforming Nvidia (NASDAQ:NVDA), which has recovered from a 22% drop in January to sit at just 10% below its highs. While Nvidia’s AI dominance remains unchallenged, AMD’s expanding data center business, growing demand for Instinct MI300 AI GPUs, and the upcoming MI350 product launch in mid-2025 raise the question: is AMD an undervalued AI play?

The China trade risk is a major factor affecting AMD, given that 23% of its revenue is tied to China, compared to Nvidia’s 14% exposure. With a potential Trump administration reintroducing aggressive tariffs, investors fear the company’s growth momentum could be impacted. Yet, AMD’s competitive pricing strategy and cost-effective AI chips have helped it secure major clients, including Meta (NASDAQ:META) and Microsoft (NASDAQ:MSFT), which use its MI300X chips to power AI models like Llama 40B and GPT-4 Copilot.

Despite recent volatility, AMD’s fundamentals remain strong. The company reported record Q4 revenue of $7.7 billion, up 24% year-over-year, driven by 69% growth in data center revenue and 58% growth in client computing. While Q1 2025 guidance suggested a 7% sequential decline in data center revenue, a trend typical of AMD’s quarterly fluctuations, the long-term growth trajectory appears intact. However, the decision by CEO Lisa Su to stop providing AI chip revenue forecasts has left some investors uneasy.

Is AMD Closing the AI Gap With Nvidia?

AI acceleration is the primary battleground for AMD and Nvidia, with both companies vying for dominance in the data center GPU market. Currently, Nvidia generates 88% of its revenue from AI-driven data centers, while AMD’s data center segment accounts for 50% of total revenue.

While Nvidia’s H100 GPU outperforms AMD’s MI300X by 7% in Llama 70B inference benchmarks, AMD remains competitive on price-to-performance. The MI350 series, set to launch in mid-2025, is expected to deliver a 35x improvement in AI computing compared to CDNA 3, positioning AMD as a strong alternative for hyperscalers looking to diversify beyond Nvidia.

In gaming and consumer GPUs, AMD’s Radeon 7900 XTX competes against Nvidia’s RTX 4090 and 5090. The RTX 4090 is 46% faster but costs 89% more, while the RTX 5090 is 103% faster but costs 156% more, underscoring AMD’s value-driven approach.

The key disadvantage for AMD remains Nvidia’s CUDA ecosystem, which provides a full-stack AI solution that integrates hardware, software, and networking. Nvidia has achieved a 12x performance gain over the last 4.5 years, outpacing Moore’s Law and making it harder for competitors to challenge its AI dominance. While AMD cannot currently match Nvidia’s ecosystem, its aggressive pricing strategy and competitive GPU offerings ensure that it remains a viable alternative.

Is AMD Stock Undervalued?

A Discounted Cash Flow (DCF) analysis suggests that AMD needs to achieve 23% annual revenue growth over the next eight years to justify its current valuation. Given that the global GPU market is projected to grow at 28.6%-33.2% annually, and CPUs at 15.2%, AMD’s realistic growth rate is estimated at 27.8%.

Applying these growth assumptions, AMD’s fair value reaches $234 billion, implying that the stock is currently undervalued by 34%.

Current Market Cap: $174 billion

DCF Fair Value Estimate: $234 billion

Stock Price Fair Value Estimate: $180 per share

Potential Upside: 34%

Can AMD Sustain Its Growth Trajectory?

Despite strong momentum in data center and AI GPU sales, several risks remain. The semiconductor industry is highly cyclical, and supply-demand imbalances could pressure margins. If AI chip demand slows, AMD’s 23%+ required growth rate may become difficult to sustain.

Additionally, competition from custom AI silicon developed by hyperscalers like Amazon (NASDAQ:AMZN) and Google (NASDAQ:GOOGL) could erode AMD’s market share. While AMD’s CDNA architecture offers flexibility and programmability, the rise of in-house AI chips could limit AMD’s long-term growth potential.

Final Verdict – Is AMD a Buy, Sell, or Hold?

Despite Nvidia’s dominance in AI, AMD’s undervalued stock price, strong data center growth, and upcoming MI350 launch make it an attractive investment. At $125 per share, AMD trades at a discount to its DCF fair value of $180, suggesting a 34% upside potential.

While Nvidia remains the AI leader, AMD provides a cost-effective alternative for AI computing. Given its long-term growth potential, AMD is a BUY for investors seeking exposure to AI-driven semiconductor expansion at a discounted valuation.