NASDAQ:MELI: Will MercadoLibre Keep Climbing or Is a Pullback Coming?

MercadoLibre’s Explosive Growth: Can NASDAQ:MELI Maintain Momentum?

MercadoLibre Inc. (NASDAQ:MELI) has seen a remarkable surge in 2025, driven by a combination of strong e-commerce expansion, aggressive fintech growth, and improving macroeconomic conditions in Latin America. The stock has rallied over 36% from its lows, significantly outperforming broader markets. However, with valuations stretching, insider selling on the rise, and a historically volatile trading pattern, investors are questioning whether MELI stock can push past $3,000 or if a correction is imminent.

E-commerce Growth Drives MercadoLibre’s Dominance in Latin America

MercadoLibre's gross merchandise volume (GMV) hit $14.5 billion, marking an 8.2% YoY increase, despite currency headwinds from Brazil and Mexico. Excluding forex impacts, GMV growth stands at 56% YoY, indicating strong consumer demand across key markets. Notably, Argentina's GMV skyrocketed by 141%, contributing to overall outperformance as economic conditions in the region improve.

Beyond GMV, MercadoLibre reported 67.3 million unique marketplace buyers, up 12.9% YoY, with items sold per buyer increasing to 7.83 units, demonstrating growing user engagement. In logistics, 95.1% of shipments were completed through MELI's managed network, showcasing the efficiency of its fulfillment infrastructure.

Fintech Surge: Mercado Pago’s Expansion Fuels MELI’s Profitability

Mercado Pago, MELI’s fintech arm, has become a major revenue driver, with total payment volume (TPV) soaring to $59 billion (+16.3% QoQ, +4.4% YoY). Credit expansion remains a focal point, with Mercado Pago’s loan portfolio up 77% YoY, and credit card issuance skyrocketing by 172% YoY. This explosive fintech growth puts MELI in direct competition with Latin American banking giants like Nu Holdings (NYSE:NU) and Itaú Unibanco (NYSE:ITUB).

The assets under management (AUM) for Mercado Pago surpassed $10.6 billion, up 129% YoY, reflecting the platform’s increasing adoption as a primary financial service provider. More users are not just making purchases but also using Mercado Pago for everyday banking needs, a key indicator of long-term customer retention.

Profitability Soars: Will MELI Maintain Its Margin Expansion?

MercadoLibre delivered Q4 revenue of $6.06 billion, representing 42.2% YoY growth, with adjusted EPS climbing 58.6% YoY to $12.61. EBIT margins surged to 13.5% (+3 points QoQ, +8 YoY), a significant expansion driven by improved logistics efficiency and a higher-margin revenue mix, particularly in fintech and advertising.

Mercado Ads, MELI’s advertising business, reported 88% YoY FX-neutral growth, contributing to the higher 3P take rate of 20.8%. The company continues to capitalize on its vast e-commerce ecosystem by monetizing sellers through increased ad spending and promotional tools.

Insider Selling and Valuation Concerns: Is a Pullback Coming?

Despite the strong financial performance, NASDAQ:MELI insiders have been selling shares in recent months. This raises concerns about whether the stock is approaching overvaluation, especially as it trades at a forward P/E of 49.1x and a PEG ratio of 1.61x. While still competitive compared to Amazon (NASDAQ:AMZN) at 1.59x PEG, MercadoLibre’s valuation appears stretched relative to Sea Limited (NYSE:SE) at 0.79x and Alibaba (NYSE:BABA) at 0.84x.

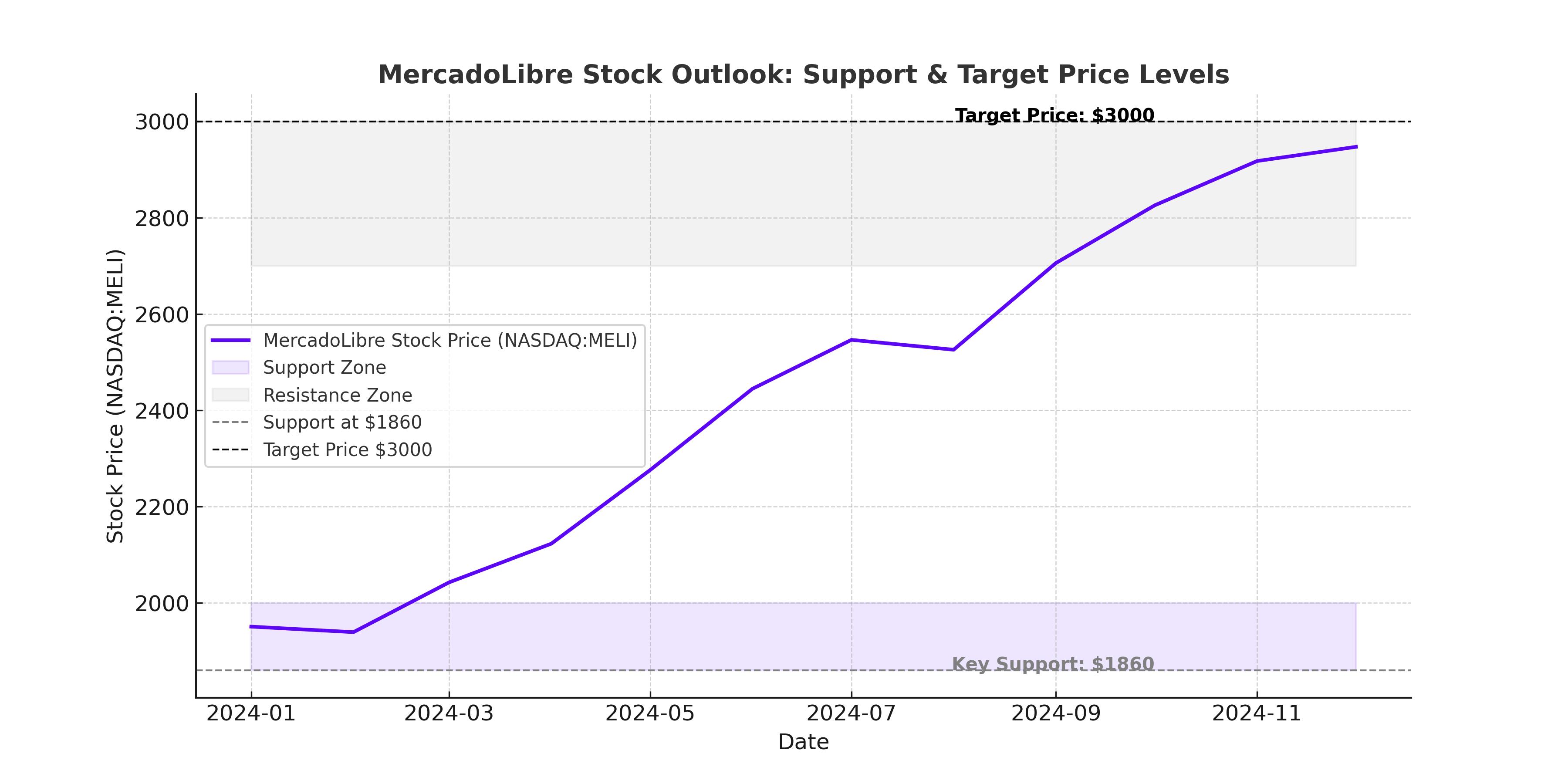

Furthermore, historical trading patterns suggest that MELI could retrace to its 200-day moving average (~$1,860), implying a potential 17.6% downside before resuming its uptrend. Investors should monitor whether the stock can sustain its current trajectory or if profit-taking could trigger a correction.

Macroeconomic Tailwinds: Latin America’s Growth Story Supports MELI

The LatAm region is recovering from previous recessions, with inflation cooling and economic growth stabilizing. MercadoLibre benefits from a resilient labor market, supporting discretionary spending and digital payments. Brazil and Mexico, its two largest markets, continue to see double-digit fintech adoption rates, providing a long runway for further expansion.

Additionally, regulatory shifts in Argentina under President Javier Milei have spurred investor optimism, particularly as the government adopts more pro-business policies. This shift has translated into a sharp recovery in Argentine GMV growth, which had previously lagged due to currency devaluations and economic instability.

NASDAQ:MELI Price Target: Can the Stock Hit $3,000?

Analysts have revised their 2025 EPS estimates upward, now expecting $8.22 in Q1, $11.04 in Q2, $11.78 in Q3, and $13.78 in Q4, reflecting higher margin expansion. Based on forward estimates, MELI's long-term price target now stands at $3,910, implying a 73% upside from current levels.

However, short-term price action remains uncertain. With technical indicators suggesting resistance at $2,700 and potential support near $1,860, traders must decide whether to buy now or wait for a pullback.

Buy, Sell, or Hold? The Verdict on NASDAQ:MELI

MercadoLibre remains a high-growth stock with strong fundamentals, but the recent 36% rally has priced in much of its upside in the short term. Given insider selling and potential resistance levels, a near-term pullback to $1,860 could present a better entry point. Long-term investors, however, may still find MELI attractive given its dominant LatAm market position, fintech momentum, and expanding margins.

Bottom Line: NASDAQ:MELI is a Buy on Dips, Hold for Now, and a Strong Long-Term Growth Play.