Nvidia (NASDAQ:NVDA) Stock Plunges 17% – Is This a Buying Opportunity Amid AI Growth?

NVDA’s 17% Sell-Off – Overreaction or Genuine Concern?

Nvidia (NASDAQ:NVDA) saw its stock price plummet 17% after DeepSeek claimed it developed a powerful AI model at a fraction of the cost of OpenAI’s GPT-4. This triggered market-wide panic, with investors questioning whether demand for Nvidia’s AI chips might decline if AI models become significantly more efficient. Despite this, NVDA has rebounded by about 10%, and analysts continue to project strong revenue growth. With its powerful AI ecosystem, unmatched CUDA software dominance, and new Blackwell chips ramping, the key question remains: is Nvidia stock undervalued after this dip, or are investors missing a larger AI industry shift?

AI Spending and OpenAI’s Stargate Project Confirm Demand for Nvidia’s Chips

While DeepSeek’s claims sparked fears that AI training costs might fall dramatically, major AI firms continue ramping up data center investments. OpenAI’s CEO Sam Altman dismissed the idea that AI models will require less compute power, stating that "more compute is more important now than ever before." OpenAI has even initiated the $500 billion Stargate AI data center project, a move that clearly signals an insatiable demand for high-performance AI chips—demand that Nvidia is best positioned to supply.

Beyond OpenAI, the United Arab Emirates recently announced a $50 billion investment into AI infrastructure in France, while multiple European countries are building new AI data centers. These developments reinforce that AI adoption isn’t slowing—it’s accelerating. Nvidia remains at the center of this boom, further solidifying its long-term bullish case.

Blackwell GPUs – The Next Growth Driver for NVDA Stock?

Nvidia’s next-gen Blackwell GPUs, launched in early February, represent a massive step forward in AI acceleration. These chips offer a significant leap in efficiency, slashing training times for AI models that previously took weeks or months. Blackwell chips have already been delivered to major partners, and Nvidia is racing to scale production. CEO Jensen Huang described demand as "staggering," with supply unable to keep up.

This new chip lineup follows the blockbuster H100 and H200 GPUs, which drove Nvidia’s data center revenue up 112% year-over-year in Q3 2025 to a record $30.8 billion. Despite some fears of AI cost reductions, Nvidia’s rapid innovation cycle means its GPUs remain the gold standard for AI training and inference.

AMD (NASDAQ:AMD) Still Lags Behind Despite Competitive Pricing

The Nvidia vs. AMD (NASDAQ:AMD) battle in AI chips is still one-sided. While AMD’s MI300X GPUs offer slightly better price-to-performance metrics, Nvidia’s dominant CUDA software ecosystem ensures it remains the AI industry’s top choice. The AI boom isn’t just about raw chip performance—developers, hyperscalers, and enterprises are locked into Nvidia’s ecosystem, making a mass exodus unlikely.

Adding to AMD’s struggles, the company recently failed to provide AI revenue guidance, sparking concerns about its growth trajectory. While Nvidia continues expanding its lead, AMD is still trying to establish itself as a viable alternative.

China Export Risks – Will New U.S. Tariffs Hurt Nvidia?

A significant risk facing Nvidia is potential new U.S. restrictions on AI chip exports to China under a second Trump presidency. China accounted for 14% of Nvidia’s total data center revenue in 2024, down from 19% in 2023 due to previous restrictions. While China remains an important market, Nvidia has successfully shifted focus to other regions, including Europe and the Middle East.

In Q1 2025, Nvidia expects China to contribute only "mid-single-digit" revenue percentages, indicating that even worst-case scenarios won’t derail overall growth. However, further tightening of U.S. trade policies could put additional pressure on NVDA’s Chinese sales.

Nvidia’s Cash Reserves and R&D Spending Outmatch AMD

One of Nvidia’s biggest strengths is its ability to outspend rivals on innovation. With $38.49 billion in cash and just $8.46 billion in debt, Nvidia has the financial firepower to continue aggressive R&D investments.

By comparison, AMD has significantly less free cash flow and is dealing with inventory build-up issues. Nvidia’s ability to spend heavily on product development ensures it maintains leadership in AI hardware, making it difficult for competitors to catch up.

Valuation: Is NVDA Stock Undervalued After the Sell-Off?

Despite its dominance, Nvidia is still trading at a forward P/E ratio of 52.44, higher than the information technology sector’s median of 32.63. However, Wall Street analysts expect NVDA’s forward P/E to shrink fivefold by 2028, making the stock look far more attractive in a long-term growth scenario.

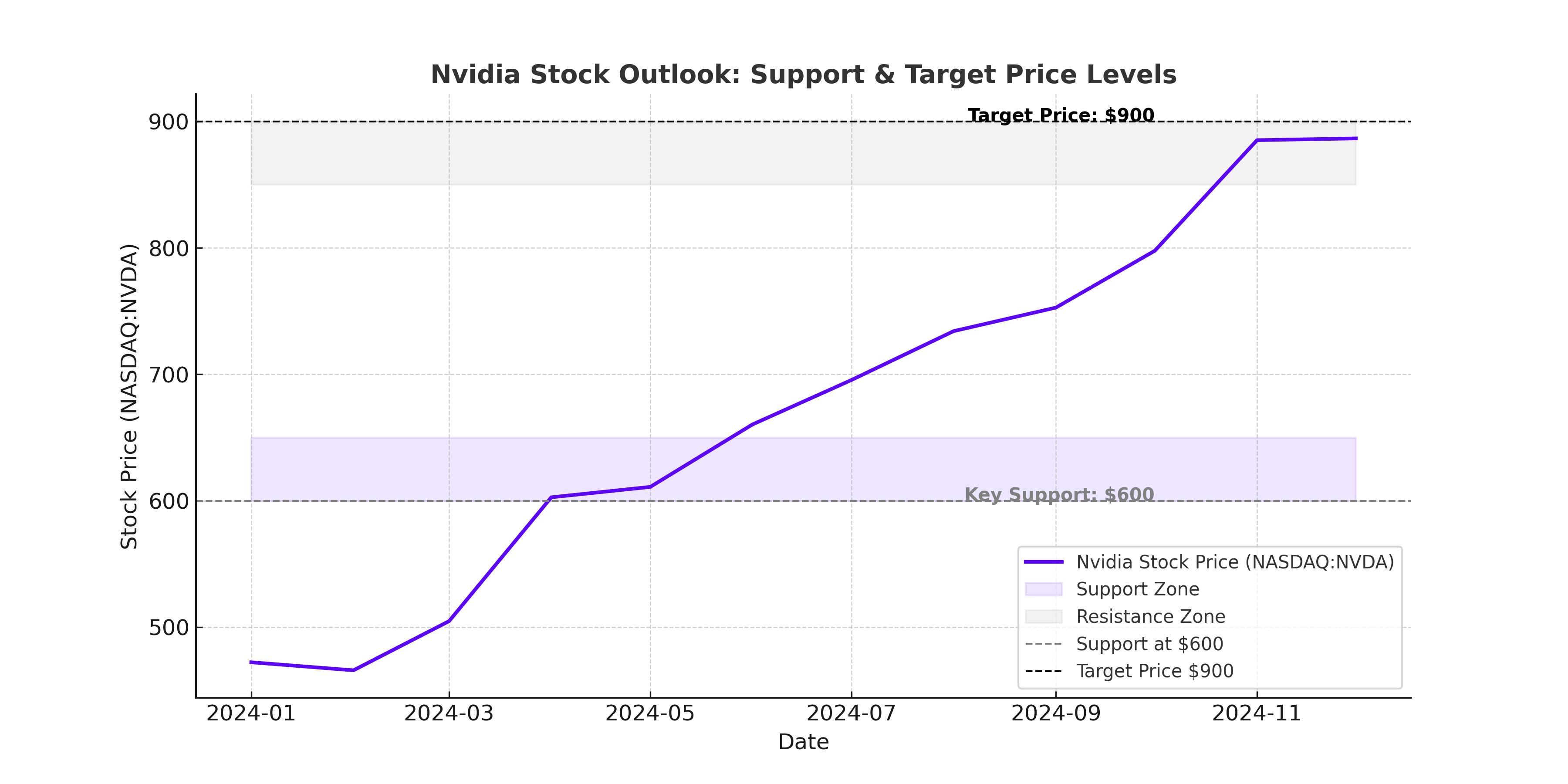

Using a Discounted Cash Flow (DCF) model, Nvidia’s fair value is estimated at $227 per share—indicating a 71% upside from current levels. Even with a more conservative growth outlook, NVDA appears at least 19% undervalued.

Key Risks: Geopolitics and AI Competition

While Nvidia remains the leader in AI acceleration, several risks need to be monitored:

- China trade tensions could impact revenue, though Nvidia has already reduced its exposure.

- Cloud spending slowdowns from major tech giants could weigh on AI chip demand, though OpenAI and Amazon have indicated increased 2025 spending.

- Emerging competition from custom AI chips developed by Amazon, Google, and Meta could pose a threat, but none currently match Nvidia’s software-hardware ecosystem.

Conclusion: Is NVDA Stock a Buy After Its 17% Drop?

Despite concerns over AI cost reductions, Nvidia remains the clear leader in the AI computing revolution. The rapid expansion of AI data centers, growing demand for Blackwell chips, and Nvidia’s dominance in CUDA software ensure its long-term strength. The recent 17% sell-off appears overblown, and with analysts maintaining a $227 price target, NVDA stock looks undervalued with a 71% upside potential.

For long-term growth investors willing to tolerate some volatility, Nvidia (NASDAQ:NVDA) remains a strong buy. View real-time NVDA stock data here: Nvidia Stock Chart