NASDAQ:QCOM – Is Qualcomm Stock Undervalued or About to Surge Past $180?

At $155, Is Qualcomm the Best AI Chip Stock to Buy Right Now? | That's TradingNEWS

NASDAQ:QCOM Stock Analysis – Is Qualcomm a Buy as AI and Edge Computing Take Over?

Qualcomm (NASDAQ:QCOM) has been at the center of the semiconductor industry’s transformation, with AI-driven edge computing, IoT expansion, and automotive chip dominance driving future growth. Despite a recent 8% pullback, Qualcomm reported record revenue of $11.7 billion in Q1 FY25, marking an 18% YoY increase. However, concerns over Apple's (NASDAQ:AAPL) shift to in-house modem production and a struggling smartphone market have led to mixed investor sentiment.

The key question: Can Qualcomm offset the Apple modem loss and capitalize on the growing AI chip market to drive long-term stock gains?

AI-Powered Edge Computing Positions NASDAQ:QCOM for Long-Term Growth

Qualcomm is rapidly positioning itself as a leader in portable AI, a shift from traditional cloud-based computing to on-device AI processing. The recent emergence of efficient AI models like DeepSeek has accelerated demand for on-device AI chips, making Qualcomm’s Snapdragon processors a critical piece of next-gen computing.

CEO Cristiano Amon has emphasized that AI inference is moving to the edge, meaning smartphones, IoT devices, and autonomous systems will process AI locally rather than relying on cloud infrastructure. This shift allows faster processing, lower latency, and increased security, which is key for AI-powered applications like self-driving cars, real-time translation, and smart assistants.

During the Q1 earnings call, Amon stated:

"We remain very optimistic about the growing edge AI opportunity across our business. AI models are becoming smaller, more capable, and now able to run directly on-device. With the industry’s most powerful and efficient AI processors, we’re well positioned to drive this transition."

This signals a fundamental shift in computing, and Qualcomm stands to profit immensely from this trend.

Q1 FY25 Earnings: Record Revenue, Strong EPS Growth, and Market Skepticism

Qualcomm’s latest earnings report exceeded expectations, yet the market reacted with caution. The company posted an EPS of $3.41, beating estimates by $0.42 per share, a 14% surprise. Revenue came in at $11.67 billion, surpassing expectations by $730 million.

Smartphone chip revenue remains Qualcomm’s largest segment, accounting for $7.57 billion, a 13% YoY increase. Notably, Qualcomm secured 100% of modem supply for Samsung’s Galaxy S25, strengthening its premium smartphone dominance.

IoT revenue surged 36% YoY to $1.5 billion, while automotive revenue hit a record $961 million, up 61%. Qualcomm’s Snapdragon Digital Chassis is now embedded in top automakers, setting the stage for autonomous vehicle dominance.

Yet, despite these wins, Qualcomm’s stock dropped post-earnings, as analysts focused on its future risks rather than its strong financials.

Apple’s Move to In-House Modems – A $7.7 Billion Revenue Hit?

Apple’s decision to phase out Qualcomm’s modems by 2027 has raised concerns about a significant revenue loss. Apple currently contributes an estimated $7.7 billion per year in modem sales to Qualcomm, making up 22% of total revenue.

While Apple acquired Intel’s modem division in 2019, it has struggled to develop a competitive 5G modem. Bloomberg reports that Apple’s in-house modem lacks mmWave support, is slower than Qualcomm’s Snapdragon X70, and does not support key carrier technologies.

Despite Apple’s efforts, Qualcomm extended its modem contract with Apple through 2026, and industry experts remain skeptical that Apple will successfully replace Qualcomm’s chips in the near future.

Even if Apple fully transitions to its own modems, Qualcomm’s diversified revenue from AI, automotive, and IoT markets should offset the decline. The company is rapidly reducing its reliance on smartphone revenue, ensuring long-term stability.

Is the Smartphone Market a Risk for NASDAQ:QCOM?

Qualcomm’s core smartphone business is under pressure as global smartphone shipments have declined 19% since 2017. Consumers are holding onto their devices longer, with the average replacement cycle now exceeding 36 months.

Used smartphone sales have skyrocketed, making up 22% of the total market, further limiting new device demand. Additionally, in China, Huawei’s resurgence has put pressure on Apple and foreign smartphone makers, leading to a 57% decline in foreign brand sales in Q4 2024.

Despite this challenging macro environment, Qualcomm’s premium smartphone strategy is working. The company controls 100% of modems in Samsung’s flagship models, and its AI-powered chips are becoming essential for high-end devices. While smartphone sales may decline, Qualcomm is capturing more revenue per device, boosting margins.

Automotive and IoT Growth – Qualcomm’s Future Revenue Engines

Qualcomm’s automotive revenue has now hit six consecutive record quarters, growing 61% YoY to $961 million. The company has secured partnerships with Hyundai, General Motors, and Amazon, solidifying its dominance in AI-powered vehicle technology.

A partnership with AWS will allow Qualcomm to integrate AI-powered in-vehicle experiences, reducing development time and costs for automakers. With the automotive industry moving toward software-defined vehicles and autonomous driving, Qualcomm’s Snapdragon Digital Chassis is becoming an industry standard.

Meanwhile, the IoT segment grew 36% YoY, reaching $1.5 billion in Q1 FY25 revenue. Qualcomm launched the next-gen Qualcomm Aware Platform, which enables businesses to integrate AI-powered location tracking and monitoring solutions across multiple industries.

With IoT adoption accelerating in retail, logistics, and smart home technology, Qualcomm is tapping into a rapidly growing market.

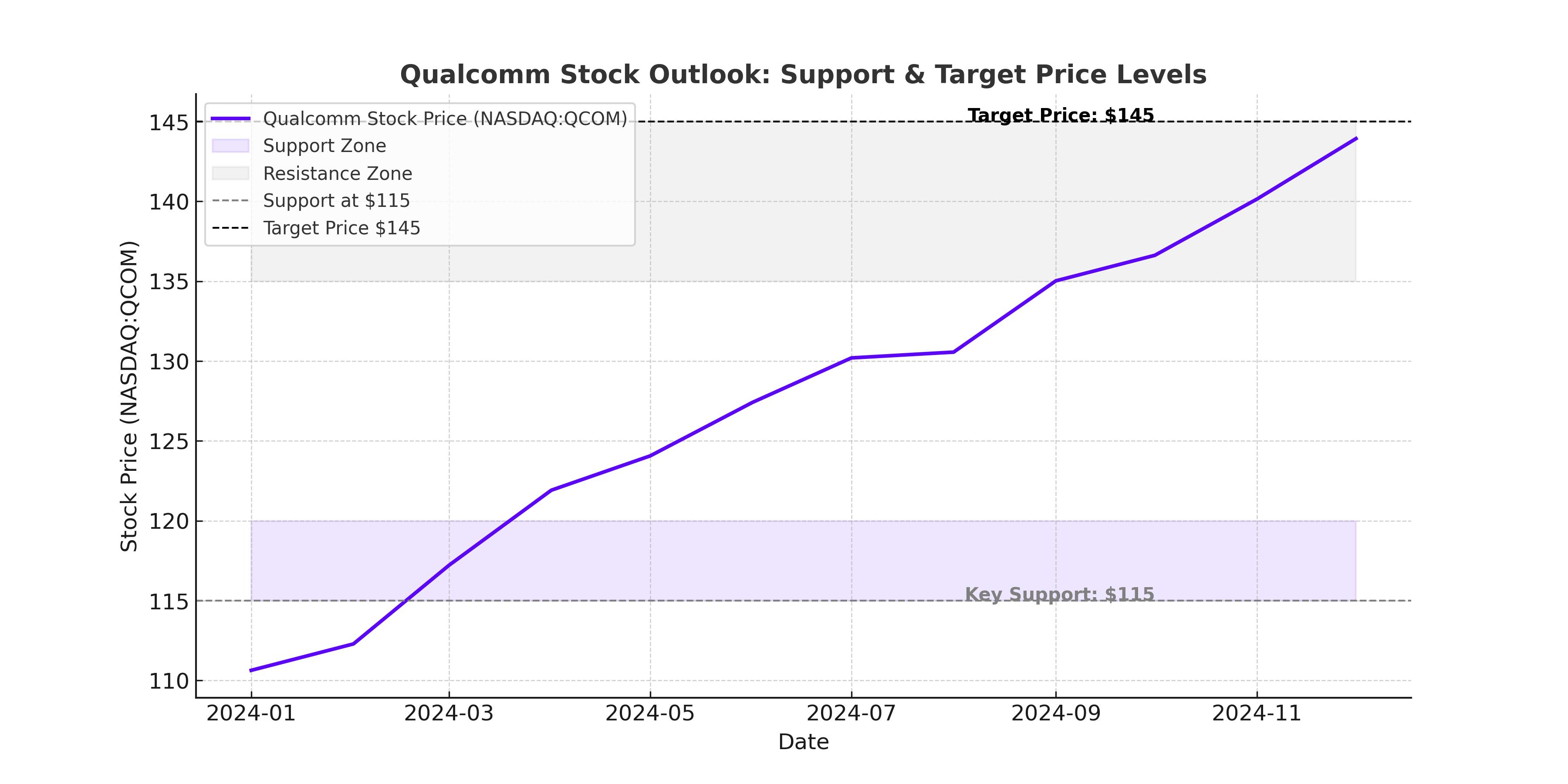

Valuation – Is NASDAQ:QCOM Undervalued?

Despite its AI leadership and record-breaking revenue, Qualcomm remains significantly undervalued compared to its tech peers.

Qualcomm’s forward P/E is just 14.7x, compared to the semiconductor sector median of 25.5x, meaning the stock is trading at a 42% discount.

Forward revenue growth is projected at 8.1%, which is 33% above the sector median, while forward EPS growth is expected to reach 13.3% YoY, outpacing the industry.

If Qualcomm’s valuation multiple expands toward the sector average, the stock has a 25.88% upside potential from current levels.

Should You Buy, Sell, or Hold NASDAQ:QCOM?

Qualcomm’s record-breaking AI revenue, growing automotive presence, and deep integration into next-gen computing make it one of the most compelling chip stocks today.

The biggest risk remains Apple’s modem transition, but even if Qualcomm loses $7.7 billion in annual revenue, its rapidly growing AI, automotive, and IoT businesses will offset the decline. The company is executing well, securing major partnerships, and driving new revenue streams in high-growth industries.

With a deeply undervalued stock, strong earnings momentum, and a long-term AI-driven growth trajectory, Qualcomm presents a strong buying opportunity at current levels. Investors looking to capitalize on the AI computing revolution should consider NASDAQ:QCOM as a top-tier tech investment.

For real-time price movements, visit Qualcomm’s stock chart.