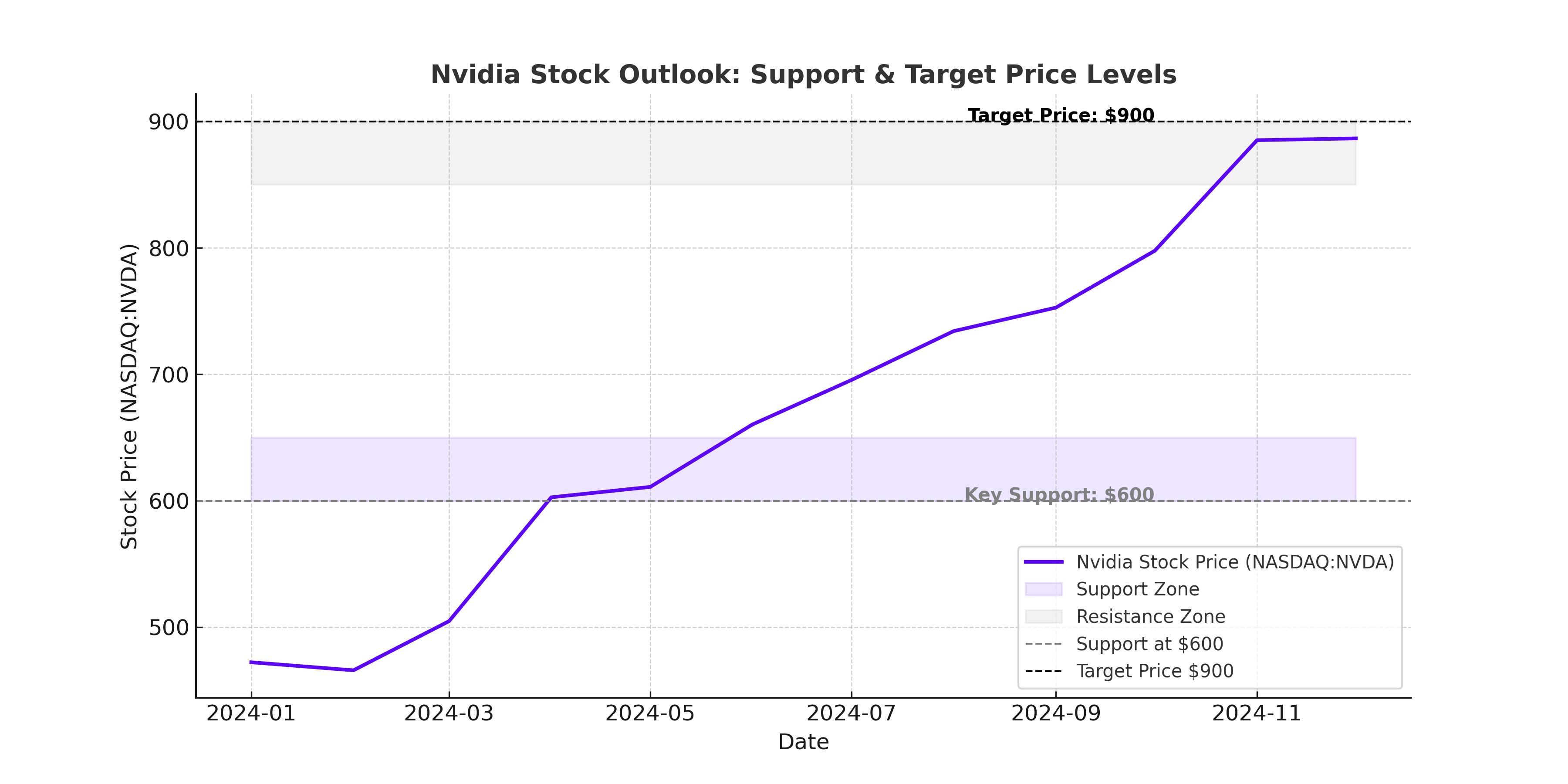

Nvidia (NASDAQ:NVDA) Stock at a Crossroads – Is AI Hype Enough to Justify a $200 Price Target?

Can Nvidia Keep AI’s Hottest Chip Business on Top, or Will DeepSeek and AMD Disrupt the Market? | That's TradingNEWS

NASDAQ:NVDA – Will Nvidia’s AI Domination Continue Amid Rising Competition and Market Uncertainty?

Nvidia (NASDAQ:NVDA) Eyes $38.16 Billion Q4 Revenue – A Critical Test for AI’s Market Resilience

Nvidia Corporation (NASDAQ:NVDA) is gearing up for a crucial earnings report on February 26, with Wall Street expecting $38.16 billion in revenue for Q4. The stock has been on a meteoric rise over the past year, fueled by its dominance in artificial intelligence chips, specifically the high-demand H100 and H200 GPUs. But as AMD (NASDAQ:AMD) gains ground with its MI300X series, China ramps up its AI independence, and US export restrictions threaten key revenue streams, investors are watching closely for any signs of a slowdown. The real test will be Nvidia’s margins, which have been soaring above 70%, a critical benchmark that signals whether its pricing power remains intact. Any dip in gross margin would suggest rising competition, cost pressures, or a potential cooling of the AI boom.

Can Nvidia (NASDAQ:NVDA) Maintain Its AI Leadership as China’s Demand Shifts?

While Chinese tech giants such as Tencent (OTCPK:TCEHY), Alibaba (NYSE:BABA), and ByteDance (private) continue to order Nvidia’s H20 GPUs, geopolitical risks remain a looming threat. The H20, a downgraded version of the H100, was specifically designed to comply with US export controls, yet it still managed to generate a staggering $12 billion in sales in 2024, with over 1 million units shipped. However, China’s move toward homegrown AI chips—spurred by initiatives like DeepSeek’s cost-efficient AI model—could pose a long-term risk.

The question for Nvidia is whether its Blackwell GPUs, set to launch later in 2025, will be enough to counteract potential revenue declines from restricted markets. If Nvidia pivots toward enterprise AI solutions to offset these risks, investors may see a new revenue model emerge beyond just hyperscaler demand.

DeepSeek’s $5.6 Million AI Training – A Real Disruptor or Just a Government-Subsidized Illusion?

A major shock to the AI industry came when DeepSeek (private) claimed it trained a GPT-4-class AI model (R-1) for just $5.6 million, significantly undercutting OpenAI’s reported $100+ million in training costs for GPT-4. At face value, this seems like a revolutionary cost reduction—but industry experts are skeptical. Training AI models requires massive computational power, massive datasets, and a highly skilled engineering team. The speculation is that China may have heavily subsidized DeepSeek’s costs, potentially providing free access to computing power, discounted electricity, and state-supported data centers.

This presents a strategic threat to Nvidia because if hyperscalers begin prioritizing cost-efficient AI training models, it could reduce demand for Nvidia’s most expensive GPUs. However, industry insiders argue that while DeepSeek’s model demonstrates efficiency, AI still fundamentally requires massive computational power—and Nvidia’s CUDA ecosystem remains unmatched in performance and scalability.

Can Nvidia (NASDAQ:NVDA) Defend Its Market Share as AMD’s MI300X Gains Traction?

Competition is heating up from AMD (NASDAQ:AMD), which has aggressively positioned its MI300X GPUs as a direct competitor to Nvidia’s H100 series. Recent benchmarks suggest the MI300X performs well in inference tasks and is priced more competitively than Nvidia’s flagship AI accelerators. Major cloud providers like Microsoft (NASDAQ:MSFT) and Meta (NASDAQ:META) have already begun testing and deploying AMD’s AI chips, signaling a potential diversification away from Nvidia’s dominance.

However, Nvidia still holds the software advantage—its CUDA platform remains the standard for AI development, giving it a critical ecosystem moat that AMD has yet to penetrate fully. Unless AMD can offer a seamless alternative to CUDA, Nvidia is likely to maintain its lead in AI hardware adoption.

Will Nvidia’s Q4 Earnings Justify Its $200 Price Target?

Wall Street analysts remain divided on whether Nvidia’s current valuation justifies its forward growth potential. The company’s net income is projected to hit $19.18 billion for Q4, with a net margin of 51.16%. While this is slightly lower than the 55.5% TTM net margin, it remains one of the most profitable tech companies in the world.

Nvidia’s Q4 guidance will be the key market-moving factor. If the company raises its Q1 2025 forecast, expect a surge in buying activity that could push NVDA toward the $200 price target. However, if Nvidia warns of AI demand cooling, the stock could see a near-term correction.

Is Nvidia (NASDAQ:NVDA) a Buy, Sell, or Hold?

Despite growing competition, Nvidia remains the undisputed AI chip leader, and hyperscaler CapEx is still projected to grow to a record $325 billion in 2025. The company’s ability to navigate China’s shifting demand, DeepSeek’s disruptive claims, and AMD’s rising competition will determine whether it remains the dominant force in AI hardware.

With Nvidia’s valuation still showing an upside of at least 25%, long-term investors may view any earnings-related pullbacks as a buying opportunity. However, short-term traders should brace for volatility, particularly if Nvidia’s margins show early signs of compression. Investors should closely monitor Nvidia’s guidance, hyperscaler demand, and GPU pricing trends as key indicators of future growth.

Check Nvidia's real-time stock chart here: NASDAQ:NVDA Real-Time Chart

Track insider transactions and company profile updates here: NASDAQ:NVDA Insider Transactions