NYSE:GIS – Is General Mills Stock Undervalued or Stuck in a Low-Growth Trap?

At $59, Is GIS Stock a Buy Before a Recovery or a Value Trap? | That's TradingNEWS

NYSE:GIS – Is General Mills Stock a Strong Buy or a Low-Growth Trap?

General Mills (NYSE:GIS) Faces Stagnant Growth but Strong Cash Flow – What’s Next?

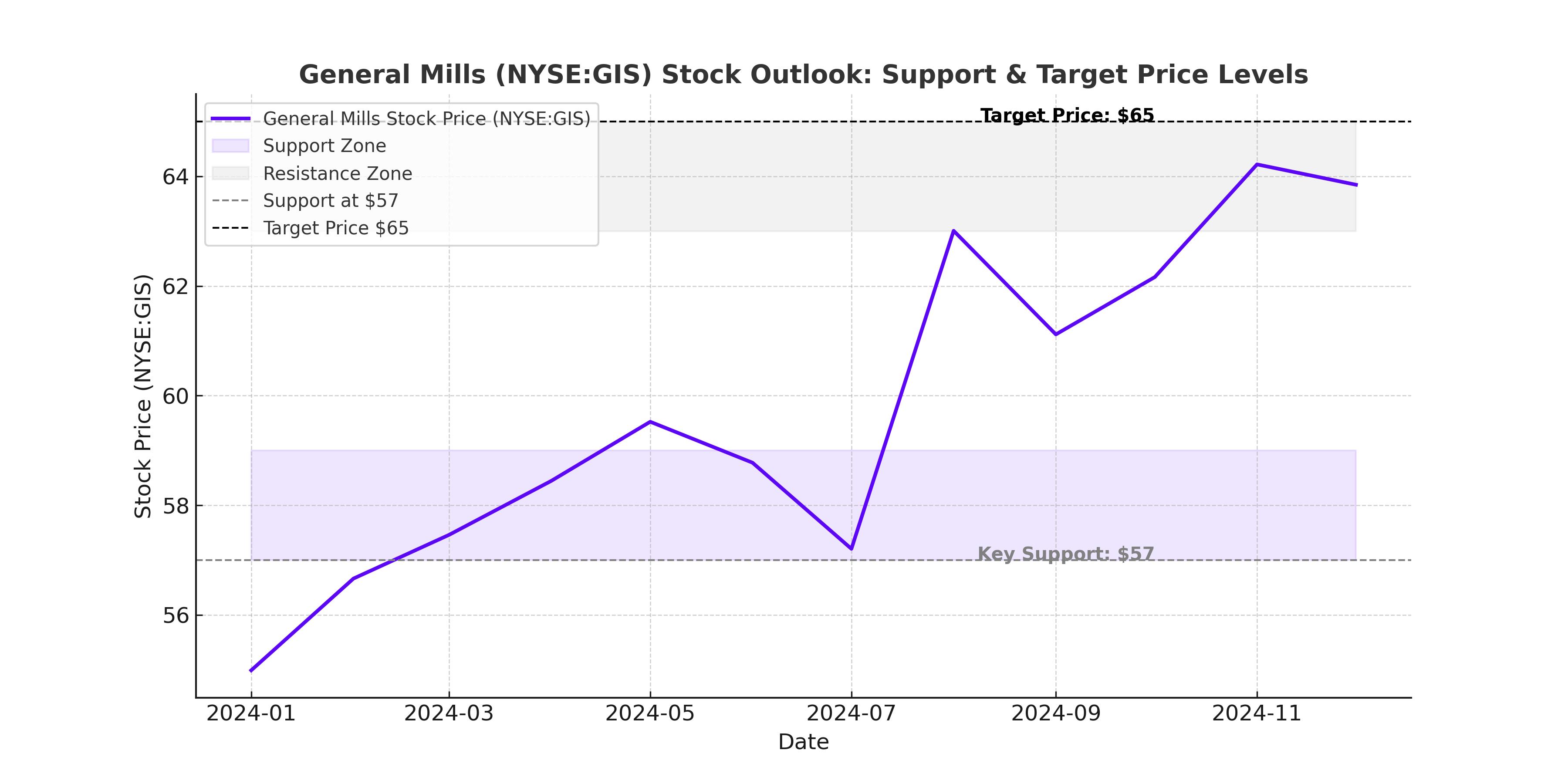

General Mills (NYSE:GIS) is trading at $59.32, hovering near its multi-year lows, yet its fundamentals show resilience. With a 4% dividend yield and a forward P/E of 13.5, the stock looks undervalued compared to historical norms and industry peers. But the question remains—can GIS break out of its sluggish revenue growth and justify a higher valuation?

While the S&P 500 surged over 34% in the last two years, GIS stock has dropped 0.9%, reflecting investor uncertainty about its ability to drive meaningful growth. Management has been actively restructuring the business, offloading weaker segments like its yogurt division and doubling down on pet food and frozen meals. The company is also navigating pricing pressures and shifting consumer habits, which have impacted volume sales.

GIS Revenue Growth – A Struggle to Maintain Momentum

GIS reported $19.86 billion in revenue for 2024, a 1.1% decline from 2023, marking a slowdown despite a 2% boost from price increases. The real issue? Volume declines continue to weigh on sales, as more consumers shift toward private-label brands and discount alternatives. This trend is visible across the packaged food industry, but GIS’s ability to offset the weakness through higher pricing has its limits.

Breaking it down by category, GIS’s Pet Food segment has shown strong growth, with brands like Blue Buffalo rebounding after targeted pricing adjustments and increased marketing. The North America Foodservice division also grew 8% YoY, fueled by demand for frozen baked goods and bulk food supplies. But international sales, particularly for Häagen-Dazs in China, have plummeted by double digits, with store traffic declining and economic pressures limiting expansion.

Looking ahead to 2025, management expects flat organic revenue growth, a revision from its earlier projection of 0%-1% growth. Worse, EPS guidance was also cut to a decline of 2%-4%, largely due to the divestiture of the yogurt business. This restructuring is expected to bring in $2.1 billion in cash, giving GIS financial flexibility, but it does little to address near-term growth concerns.

Profitability and Cash Flow – GIS Is Still a Cash Machine

While revenue growth remains weak, GIS has done a solid job expanding margins and controlling costs. Operating income for Q2 grew 7% YoY to $1.1 billion, driven by gross margin improvements of 250 basis points to 36.9%. The company’s cost-cutting efforts and supply chain optimizations have been effective, helping stabilize profits even as sales remain sluggish.

Operating cash flow remains strong at $3.29 billion, a significant improvement from $2.83 billion in 2023. Adjusted net income also climbed 8.1% YoY to $2.64 billion, proving that GIS is still generating stable earnings. However, with its $12.23 billion debt load, General Mills will need to prioritize debt reduction in the coming quarters, potentially limiting aggressive share buybacks or new growth investments.

Valuation – GIS Is Cheap, but Does It Deserve to Be?

GIS stock trades at a P/E of 13.5, well below its five-year average of 17.1 and significantly lower than industry peers like The Hershey Company (HSY) at 17.7, Mondelez (MDLZ) at 20.7, and Kellanova (K) at 28.2. The stock is also undervalued on an EV/EBITDA basis, at just 10.5, compared to Kraft Heinz (KHC) at 13.9 and Mondelez at 12.5.

If GIS were to trade at even the lowest multiple of its competitors, its upside potential would be 26.3%. If it reverted to the industry average, GIS stock could see gains of up to 85%, making it one of the more attractive value plays in the consumer staples sector.

Dividend Stability – GIS Is a Reliable Income Stock

One of GIS’s strongest selling points is its 4.0% dividend yield, significantly higher than the S&P 500’s 1.4% average yield. The dividend is well-covered with a payout ratio of 51%, meaning there’s room for growth. The company has maintained five consecutive years of dividend increases, with a five-year CAGR of 4.1%.

For income investors, GIS remains an attractive choice, particularly given its defensive nature and consistent profitability. However, the lack of significant earnings growth could limit long-term dividend expansion.

Risks – Is GIS a Value Trap?

GIS faces several key risks that could keep the stock range-bound despite its attractive valuation. The biggest issue is consumer demand trends—with inflationary pressures easing, price increases will no longer be enough to drive revenue growth. Instead, GIS will need to find ways to boost volume sales, a challenge given increasing competition from private-label brands and shifting consumer preferences toward healthier, fresher alternatives.

Another risk is interest rates and economic conditions. Higher rates tend to pressure consumer staples stocks, as investors favor high-growth sectors in a rising-rate environment. GIS is particularly vulnerable because of its high debt load, which could limit financial flexibility if borrowing costs remain elevated.

Finally, international challenges remain a concern. GIS’s China segment has been a drag on growth, with double-digit declines in Häagen-Dazs retail sales. Management is restructuring operations in the region, but recovery could take time, and further macroeconomic slowdowns could worsen the situation.

Buy, Sell, or Hold – What’s the Call on GIS Stock?

At $59, GIS stock presents an intriguing opportunity. The valuation is compelling, especially relative to peers, and the dividend is safe with room for growth. The business model remains stable, and recent restructuring efforts could improve profitability in the long run.

But the lack of clear revenue growth drivers keeps GIS from being a strong buy. Until volume trends improve and international headwinds ease, the stock is likely to remain stuck in a low-growth holding pattern.

For long-term investors focused on dividends and value, GIS remains a solid buy at current levels, with limited downside risk and the potential for steady, albeit slow, appreciation. For those looking for strong growth catalysts, however, the stock may not be the best choice until clearer signs of a sales rebound emerge.