Amazon Web Services (AWS): Dominating the Cloud Market

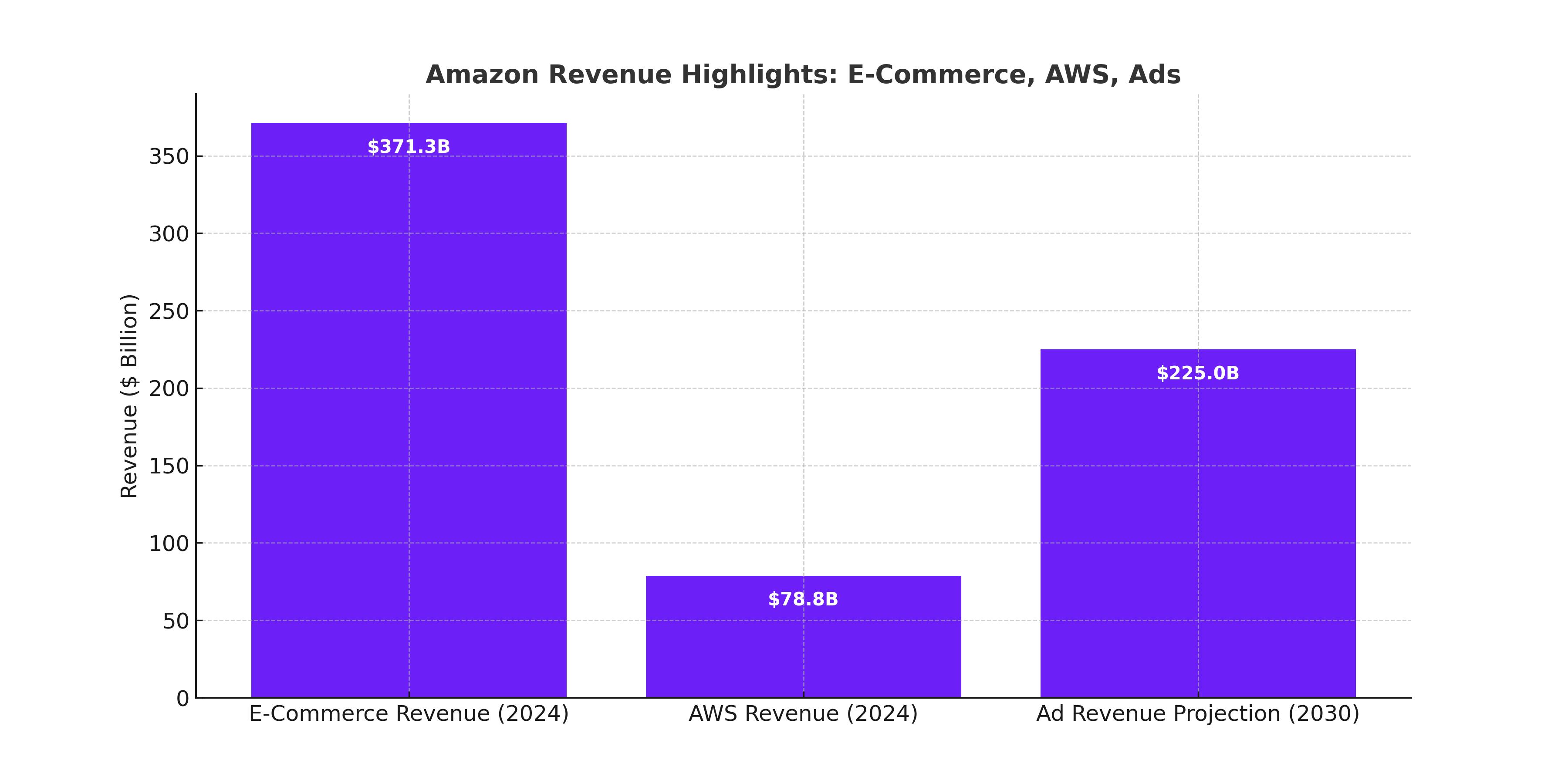

AWS remains a crown jewel for Amazon, holding 31% of the global cloud market and generating $78.8 billion in revenue in 2024. The segment’s 37% operating margin underscores its profitability. With the U.S. cloud market forecast to grow to $2.3 trillion by 2032, AWS could generate $575 billion in revenue if it retains a 25% market share. Amazon's strategic shift toward in-house custom chip manufacturing through Annapurna Labs could further elevate operating margins to 42.5%, contributing $244 billion in annual operating profit by 2032. This growth cements AWS as a $3.66 trillion business by valuation, outpacing competitors like Microsoft Azure and Google Cloud.

Digital Advertising: The Hidden Growth Engine

Amazon’s digital ad business is silently capturing significant market share, overtaking traditional leaders like Meta and Google. Holding over 15% of the global digital ad market by 2030, Amazon is projected to generate $225 billion annually in ad revenue. Given the $1.5 trillion global digital ad market forecast, this segment could be valued at over $1 trillion at a conservative EV/Sales multiple of 4x. Amazon’s ability to integrate ads into its e-commerce and Prime ecosystem creates an unmatched value proposition for advertisers. This strategic synergy is a crucial driver of its rising ad revenue.

Robust Cash Flow Fuels Aggressive Investment

Amazon generated $70.2 billion in operating cash flow during 2024, supporting $56.9 billion in capital expenditures primarily for AWS and technological infrastructure. This investment ensures sustained growth and strengthens Amazon’s competitive edge across e-commerce, cloud, and digital advertising. The company’s negotiating power with suppliers enhances its ability to optimize pricing and margins. For example, partnerships through Vendor and Seller models allow Amazon to dictate favorable terms, ensuring it remains a critical channel for consumer goods companies worldwide.

Evaluating NASDAQ:AMZN’s Valuation and Market Leadership

Amazon’s diversified revenue streams across e-commerce, AWS, and digital ads present a combined opportunity of $6.6 trillion in valuation by 2032. With e-commerce contributing $2.04 trillion, AWS adding $3.66 trillion, and digital ads reaching $1 trillion, Amazon’s growth potential remains significant. Despite these opportunities, the current EV/EBITDA multiple of 17.1x suggests limited upside compared to earlier entry points. However, as Amazon invests heavily in automation, AI, and logistics, its long-term profitability trajectory justifies a bullish outlook.

Why Is NASDAQ:AMZN a Buy Despite Competition?

Amazon (NASDAQ:AMZN) has cemented its dominance in e-commerce and cloud computing, with both segments delivering unparalleled revenue and profit growth. In 2024, the company reported $271.9 billion in North American e-commerce revenue and $78.8 billion from its AWS cloud division. AWS alone holds a commanding 31% global market share, and its operating margins reached an impressive 37%. Even in a highly competitive cloud landscape, Amazon’s ability to integrate its services with custom solutions like Annapurna Labs' chips gives it a technological edge over rivals like Microsoft Azure and Google Cloud.

Moreover, Amazon’s advertising business, often underestimated, is growing rapidly, with the potential to capture over 15% of the global digital ad market by 2030. This segment could generate annual revenue exceeding $225 billion, driving significant shareholder value. With an estimated total addressable market (TAM) for digital advertising of $1.5 trillion by the end of the decade, Amazon’s seamless integration of ads into its platforms creates a competitive advantage that others struggle to match.

While risks like macroeconomic headwinds, tighter monetary policy, and aggressive competition remain, Amazon’s ability to generate over $70 billion in operating cash flow annually ensures it can outspend competitors in key growth areas. Strategic investments in automation, robotics, and cutting-edge cloud technology position Amazon for sustained long-term growth. At current levels, NASDAQ:AMZN offers significant upside for investors willing to capitalize on its market leadership and future potential. View the real-time NASDAQ:AMZN chart here for the latest updates on its performance.

That's TradingNEWS