Palo Alto Networks (NASDAQ:PANW): AI Dominance, Platformization Strategy, and Valuation – Is It a Buy or a Bubble?

Palo Alto Networks (NASDAQ:PANW) Stock Surges, But Can It Justify a $213 Price Target?

Palo Alto Networks (NASDAQ:PANW) has been on a relentless climb, fueled by its aggressive AI-driven cybersecurity transformation and platformization strategy, which integrates security solutions into three major platforms—Network Security, Cloud Security, and Security Operations. Revenue in Q1 FY25 hit $2.14 billion, marking a 13.9% YoY increase, with Next-Gen Security (NGS) ARR skyrocketing 40% YoY to $4.5 billion. Despite these gains, concerns over valuation persist, with the stock trading at $187 and a forward P/E of 56.4x. Is PANW still a strong buy, or is a pullback looming?

AI and Platformization: The Key to Palo Alto’s Growth

Palo Alto’s "Platformization" strategy consolidates standalone cybersecurity products into comprehensive, AI-enhanced solutions, making security more efficient, scalable, and cost-effective. The three core platforms—Network Security, Cloud Security, and Security Operations—are the backbone of this transformation.

Network Security: Leading the Firewall Evolution

Palo Alto’s Strata platform, a key part of the Network Security segment, remains dominant in enterprise firewall solutions, integrating SASE (Secure Access Service Edge), Zero Trust Network Access (ZTNA), and Firewall-as-a-Service (FWaaS). This combination eliminates the need for fragmented security tools, reducing costs for enterprises.

Strata continues to see high demand, with 70% of PANW’s firewall revenue now driven by virtual firewalls. This shift underscores growing enterprise demand for cloud-based security solutions over traditional on-premise firewalls, giving Palo Alto a critical advantage against competitors like Cisco (CSCO) and Fortinet (FTNT).

Cloud Security: Prisma’s AI-Powered Expansion

Prisma Cloud, the company’s flagship cloud security platform, is gaining traction as enterprises shift to multi-cloud architectures. With AI-powered security monitoring and compliance automation, Prisma Cloud is a major driver of Palo Alto’s ARR growth.

The cloud security market is expected to grow at a 26.3% CAGR from 2024 to 2029, making it the fastest-growing segment in cybersecurity. With Prisma already holding a strong market position, Palo Alto is well-positioned to capitalize on this boom.

Security Operations: The Cortex XSIAM Revolution

Palo Alto’s Cortex XSIAM platform is a game-changer in automated security operations, offering real-time threat detection and response powered by AI. In Q1 FY25, Cortex XSIAM’s ARR grew 180% YoY, highlighting strong demand from enterprise customers looking to automate threat detection and minimize cyberattack risks.

A key driver behind this growth is the IBM QRadar acquisition, which helped Palo Alto migrate over 550 IBM QRadar SaaS customers to XSIAM, adding $80 million in bookings. With AI-driven cybersecurity threats on the rise, Palo Alto’s autonomous security solutions are becoming indispensable.

Revenue Growth and Future ARR Projections

Palo Alto’s subscription-based revenue model is proving to be a key strength, shifting the company away from a hardware-focused business and into a high-margin, recurring revenue structure.

| Fiscal Year | Revenue ($B) | Growth % |

|---|---|---|

| FY24 (Actual) | 8.02 | 14% |

| FY25 (Est.) | 9.57 | 19% |

| FY26 (Est.) | 11.43 | 20% |

| FY27 (Est.) | 13.72 | 20% |

| FY28 (Est.) | 16.53 | 20% |

| FY29 (Est.) | 19.97 | 21% |

By 2030, PANW expects to have between 2,500 and 3,500 platformized customers, a significant jump from the 1,100 reported in Q1 FY25. This shift could drive an additional $4.34 billion in ARR, solidifying Palo Alto’s leadership in next-gen cybersecurity solutions.

Insider Transactions: What Are Executives Doing?

Institutional investors continue to heavily accumulate Palo Alto shares, signaling confidence in its long-term growth. Recent insider transactions can be tracked here, providing insight into executive sentiment and major stakeholder moves.

Valuation: Is Palo Alto Networks Overpriced?

At $187 per share, Palo Alto’s valuation is becoming a major point of contention.

- Forward P/E Ratio: 56.4x, significantly above its historical 10-year median of 47.7x

- Price-to-Sales (P/S): 14.62x, higher than cybersecurity peers like Fortinet (FTNT) at 10.8x and Zscaler (ZS) at 13.4x

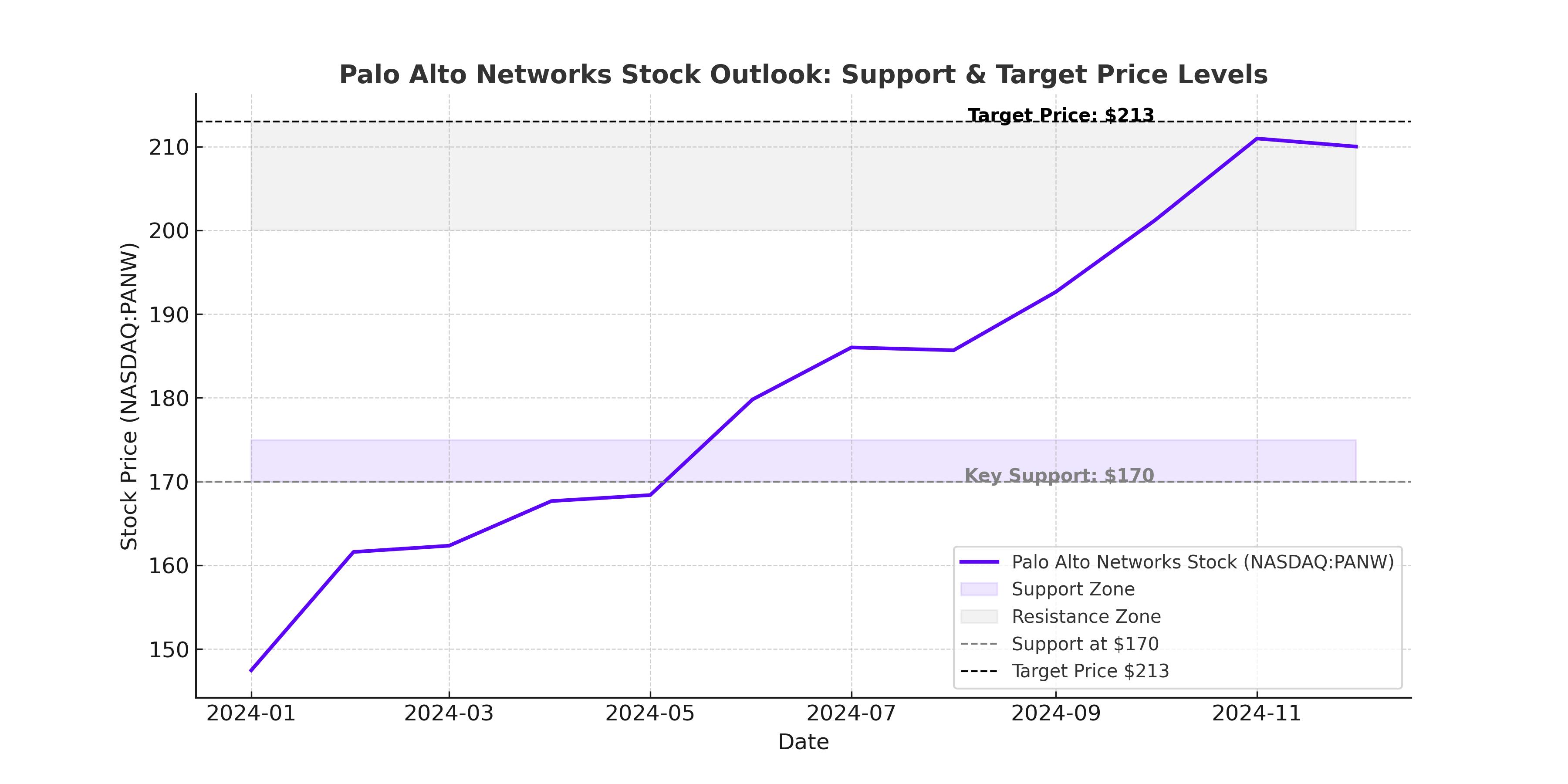

- Projected FY26 Price Target: $213, reflecting a 13.79% upside

While NGS ARR and subscription growth remain strong, any slowdown in billings or cybersecurity spending fatigue could lead to valuation compression.

Risks: What Could Derail Palo Alto’s Growth?

Despite strong fundamentals, several risks could impact Palo Alto’s long-term trajectory.

- Cybersecurity Budget Cuts: Government and enterprise cybersecurity spending remains highly cyclical, and a slowdown in IT budgets could weaken PANW’s revenue expansion.

- Increased Competition: Microsoft (MSFT), CrowdStrike (CRWD), and Zscaler (ZS) are aggressively expanding their AI-driven security platforms, threatening Palo Alto’s dominance.

- AI Hype vs. Reality: While AI-powered security solutions are boosting sales, execution remains critical. Any failure to deliver substantial improvements in threat detection or automation could dent investor confidence.

- Federal IT Spending Declines: As the U.S. government shifts budget priorities, reduced cybersecurity contracts could impact revenue.

Final Verdict: Buy, Sell, or Hold?

Palo Alto Networks remains a long-term winner in AI-driven cybersecurity, but at $187 per share, the valuation looks stretched. While the stock could hit $213 in FY26, near-term risks—budget cuts, competition, and AI execution risks—make a near-term pullback likely.

For long-term investors, buying on dips remains the best strategy. Short-term traders should watch for earnings catalysts, particularly ARR and platformization growth. Investors can track real-time Palo Alto stock movements here.

Final Call: Hold Until Further Confirmation of AI and ARR Growth

While PANW remains a leader in next-gen cybersecurity, the stock’s current valuation suggests caution. A correction to $170-$175 would provide a much stronger entry point, offering better risk-reward potential before a long-term push toward $213 and beyond.